CVS Health’s Digital Transformation: How Platform Consolidation and Agentic AI Are Building a Behavioral Data Moat

CVS Health is consolidating three businesses, Aetna, Caremark, and CVS Pharmacy, into a single AI-native engagement platform built on agentic infrastructure (Agentic Twins, Google Cloud/Gemini, and a unified consumer app) that harmonizes clinical and transactional data across the payer, PBM, and pharmacy boundary. Integrated members show a 3 to 6% drop in per-member-per-month medical costs, and the platform sits on a 185-million-consumer behavioral foundation. This case study examines how a $372.8 billion company turned fragmented post-acquisition data into a defensible moat.

Introduction

CVS Health is not digitizing healthcare, it is constructing a behavioral data platform that happens to be distributed through healthcare infrastructure. That reframing is the whole strategy. Rather than optimizing its insurance, pharmacy-benefit, and pharmacy businesses independently, CVS made the harder choice to collapse them into a single engagement layer, foreclosing quick wins in each to secure a data asset none of them could build alone.

This CVS Health digital transformation is therefore less a technology story than an architectural one. The interesting question is not which AI it deployed, but why it committed to integration over incremental improvement while under earnings pressure and mid-leadership transition. For enterprise leaders, the lesson generalizes far beyond healthcare: any company sitting on fragmented post-acquisition data faces the same decision CVS made, and the same temptation to postpone it.

Key Takeaways

- Platform over product. CVS chose to consolidate three business units into one engagement platform rather than incrementally improving each, foreclosing fast short-term wins to secure an integrated data layer no competitor can replicate.

- The data layer is the product. The unified consumer app is a data-collection mechanism as much as an experience; without harmonized back-end data, personalization is cosmetic.

- Agentic AI is the engine. Google Cloud/Gemini, Agentic Twins synthetic patient modeling, and clinician-facing AI form one of the most comprehensive agentic deployments among U.S. payer-providers.

- The constraint is organizational, not technical. Distributing decision rights across three P&Ls under HIPAA governance, mid-leadership-transition, is the real execution risk.

- The moat compounds. A 185-million-consumer behavioral foundation makes “Engagement as a Service” credible and renders dependent health-tech intermediaries obsolete with every integration milestone.

- Sequencing is the lesson. Coherent data infrastructure is the precondition for a unified interface, not its byproduct; reversing the order produces “facade integration” that collapses under load.

%20(1).png)

Let’s kickstart the conversation and design stuff people will love.

The Retail & Consumer Index

Why This Case Study Matters

The conditions that forced CVS’s hand: acquisition-driven scale, data fragmentation, margin pressure, and consumer expectations set by technology platforms outside healthcare, describe nearly every large enterprise that grew through M&A in the 2010s and now faces the compounding cost of deferred integration. CVS is simply the largest, most regulated, and most visible test of whether platform consolidation pays off.

For CEOs, CIOs, chief digital officers, and transformation leaders, the value is in the template. CVS’s 2023–2025 architecture decisions are likely to define how regulated industries approach platform consolidation for the next decade, including the uncomfortable truth that the threshold between a digitized enterprise and a platform enterprise is a discrete architectural decision, not a gradual continuum.

Strategic Context

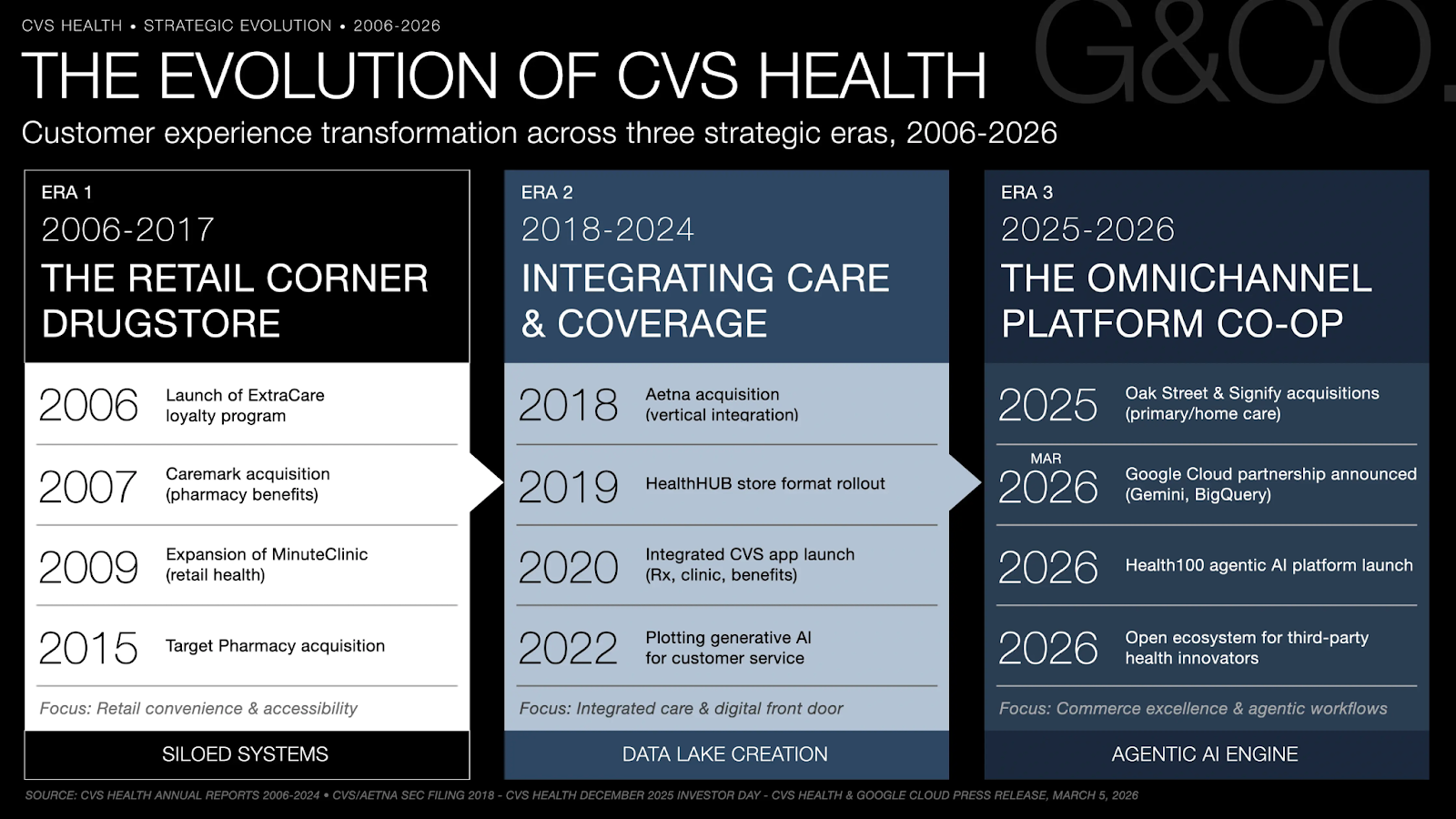

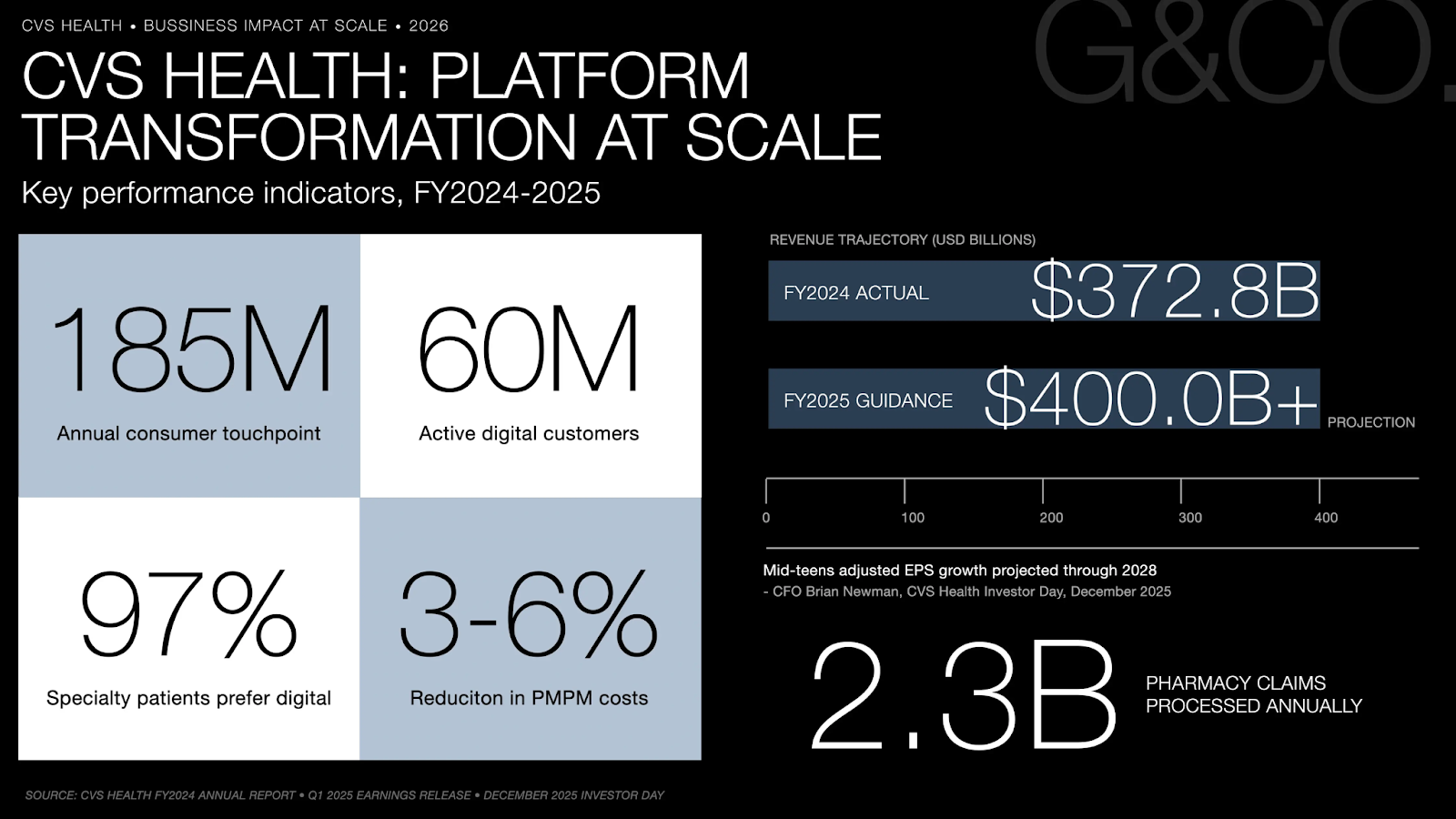

CVS enters 2026 as the largest U.S. healthcare company by revenue: $372.8B in FY2024, with Q1 2025 revenue of $94.6B already tracking toward $400B full-year guidance. Yet scale has historically been as much a liability as an advantage. The 2018 Aetna acquisition bolted a $69B payer onto a pharmacy and PBM enterprise, creating the theoretical conditions for integrated care alongside three distinct cultures, three technology architectures, and three regulatory environments under one roof.

The “Moment of Inertia” driving the strategy is not technological lag, it is identity fragmentation. A CVS Pharmacy customer, a Caremark PBM member, and an Aetna plan participant can be the same person navigating three interfaces, receiving three uncoordinated communications, and generating three disconnected data trails. That fragmentation is a structural inefficiency that prevents CVS from deploying its most valuable asset: the longitudinal behavioral and clinical data that only exists when the three units are unified. Digital transformation here is less about digitizing existing processes than about building the connective infrastructure that makes integration commercially viable for the first time.

Company Response

Between 2023 and 2025, leadership made a decisive architectural choice: prioritize platform consolidation over point-solution optimization. Improving each unit’s interface independently would have produced faster wins but permanently foreclosed the integrated data layer underpinning the long-term strategy. At the December 2025 Investor Day, CEO David Joyner framed CVS’s competitive position around making a fragmented, hard-to-navigate system simpler and more connected, with technology at the center.

The trade-off was real. Resources that could have accelerated Aetna’s margin-pressured Medicare Advantage recovery were instead directed toward infrastructure producing no immediate revenue, and high-margin Caremark operations were subordinated to an integration roadmap prioritizing consumer-experience coherence over unit autonomy. Leadership absorbed short-term earnings pressure to preserve a conviction that “Engagement as a Service” is a category-defining revenue stream unavailable to any competitor without equivalent scale.

Execution operates across four interdependent infrastructure layers:

- The Unified CVS Health App (January 2025) replaced the legacy pharmacy app with an all-in-one platform spanning CVS Pharmacy, Caremark mail-order, and CVS Specialty, integrating immunization scheduling, AI-powered medication search, spending visibility, and personalized reminders into one authenticated session. For the first time, a Caremark member and a CVS Pharmacy patient share a single digital front door.

- Agentic AI infrastructure via Google Cloud deploys Gemini multimodal models for proactive engagement, with Cloud Healthcare API and BigQuery harmonizing clinical and transactional data across units. Without this layer, personalization is cosmetic.

- Agentic Twins are AI-powered synthetic patient models built from consented behavioral data across hundreds of thousands of individuals, letting teams pressure-test workflows against simulated behavior and compress research cycles from weeks to hours.

- Clinician-facing AI tooling closes the loop: CVS Specialty patients interact with AI-supported CareTeams via secure two-way messaging, while AI-generated case-note summaries redirect clinician time from documentation toward judgment, extending the engagement loop into care delivery and generating behavioral data at every touchpoint.

Results and Evidence

The evidence concentrates in adoption scale and cost efficiency rather than immediate margin expansion, consistent with a platform investment cycle. CVS now engages 185 million consumers annually, with 60 million active digital customers as of January 2025, and processes 2.3 billion pharmacy claims a year, a transactional foundation no digital-health startup can replicate. Among CVS Specialty patients, 97% prefer digital two-way CareTeam messaging over phone, validating the engagement thesis at the population level that matters commercially.

The financial trajectory supports the thesis: FY2024 revenue of $372.8B is projected to reach $400B+ in FY2025, paired with CFO Brian Newman’s commitment to mid-teens adjusted EPS growth through 2028. The most structurally significant signal, however, is the 3–6% decrease in per-member-per-month medical costs across integrated Aetna and Caremark members over three years. That metric is the proof-of-concept for the entire integration thesis, evidence that consolidating data across the payer-PBM boundary produces measurable clinical and economic outcomes, not just UX gains.

The gaps are organizational, not technological. Three formerly autonomous P&Ls are being asked to subordinate unit optimization to a platform logic that distributes benefits unevenly over a multi-year horizon, the exact governance failure mode that sinks large transformations. Compounding it, every deployment operates where regulation treats data aggregation as a compliance risk rather than a strategic asset: HIPAA information barriers between Aetna’s claims data and CVS Pharmacy’s dispensing data demand governance architecture as sophisticated as the technology itself. The October 2024 transition from Karen Lynch to David Joyner, mid-transformation, added continuity risk, since platform efforts of this complexity are acutely sensitive to shifts in internal prioritization.

What Enterprise Leaders Can Learn

- Acquisition creates compounding data debt. CVS’s timeline reflects the true cost of resolving seven years of post-merger fragmentation, not the cost of building new technology.

- Governance must move at the speed of technology. In regulated industries, treat compliance as a deployment gate engineered alongside the architecture, not a design input that stalls investment cycles.

- Earn “Engagement as a Service” internally first. Selling external platform access before solving internal coherence exposes architectural incompleteness to your most sophisticated customers.

- Protect momentum through leadership change. Mid-transformation transitions redistribute political capital precisely when sustained commitment matters most.

- Design consumer touchpoints with data intent. An interface built without explicit data architecture becomes engagement infrastructure that cannot be monetized.

Decision Intelligence

Strategic Implications

The industry consensus frames this as healthcare digitization: an incumbent adapting to digital-native expectations. That underestimates the logic. A digitized healthcare company competes on care quality and cost; a behavioral data platform competes on data exclusivity, ecosystem lock-in, and the marginal cost of adding the next consumer or employer client to already-amortized infrastructure. CVS is building the latter.

This connects to the broader currents reshaping enterprise strategy: AI, customer experience, digital transformation, data strategy, and platform economics. The “Engagement as a Service” ambition mirrors Amazon Web Services: commercialize internal infrastructure only after proving it at internal scale, here across 185 million consumers. The organizations most threatened are not other pharmacies or insurers but the health-tech intermediaries, point solutions, digital therapeutics, engagement vendors, whose value depends on CVS’s data staying siloed. Every integration milestone eliminates a category of dependency, which is what makes the internal organizational challenge so strategically loaded: the faster CVS dissolves its silos, the more defensible its platform position becomes.

Conclusion

CVS Health crystallizes a defining tension of the current period: the organizations best positioned to build platform advantage are often the ones whose acquisition history created the most fragmented starting conditions. The Aetna deal that generated CVS’s integration complexity is the same asset that makes “Engagement as a Service” credible; no startup can replicate a 185-million-consumer behavioral foundation spanning payer, PBM, and pharmacy simultaneously.

The enduring lesson is structural. CVS is not running a conventional digital transformation: a technology upgrade layered onto an existing model. It is executing an identity transformation, converting a holding company of distinct businesses into a single platform enterprise whose moat is the data generated by their integration. The companies that should study this most closely are not healthcare companies; they are any enterprise sitting on fragmented post-acquisition data and weighing whether integration is worth the cost. CVS’s answer, playing out at $372.8B in annual revenue, is unambiguous.

Ready to explore a similar transformation?

Submit an inquiry to G&CO.Health on our contact page or click on the blue "Click to Contact Us" button on the bottom right corner of your screen for your convenience. We look forward to hearing from you.

Frequently Asked Questions

How did CVS Health execute its digital transformation strategy?

CVS consolidated Aetna, Caremark, and CVS Pharmacy into a single AI-native engagement platform across four layers: a unified consumer app, Google Cloud agentic AI infrastructure, synthetic patient modeling via Agentic Twins, and clinician-facing AI tooling that extends engagement into care delivery.

Why did CVS pursue a platform strategy rather than optimizing each business unit?

Independent optimization would have produced faster short-term gains but permanently foreclosed the integrated behavioral data layer underpinning the “Engagement as a Service” model. Leadership absorbed short-term earnings pressure to preserve platform integrity, a trade-off that only makes sense at CVS’s scale of 185 million annual touchpoints.

What is agentic AI, and how is CVS applying it in healthcare?

Agentic AI refers to systems that autonomously execute multi-step tasks without continuous human instruction. CVS applies it across consumer navigation, synthetic patient modeling, and clinician support, one of the most comprehensive agentic deployments among U.S. payer-provider enterprises.

What were the measurable results?

CVS engages 185 million consumers annually with 60 million active digital customers. Integrated Aetna and Caremark members showed a 3–6% decrease in per-member-per-month medical costs, and 97% of CVS Specialty patients prefer digital CareTeam communication. FY2024 revenue reached $372.8B with FY2025 guidance of $400B+.

What can enterprise leaders learn from it?

The core lesson is sequencing: unified consumer experiences require coherent data infrastructure as a precondition, not a byproduct. Launching integrated interfaces before solving back-end fragmentation produces facade integration that cannot scale.