Tesla’s Vertical Integration Strategy: How Owning Every Layer Turns a Car Into a Platform

Tesla owns every commercial layer of its business, the sale, the software, the charging network, the energy platform, and autonomous driving, turning the car into the entry point of a data-generating service relationship rather than a one-time transaction. The result: roughly $20.6 billion in non-automotive revenue in FY2024, energy generation and storage up 67% year over year, and $1.1 billion in recurring Full Self-Driving subscription revenue. This case study explains why owning the data infrastructure, not the front-end experience, is what creates a durable moat.

Introduction

Tesla stopped selling cars as discrete transactions and started using them as the entry point to a managed, data-generating service relationship. That shift, from selling a product to enrolling a customer, is what turned an automaker into a consumer technology platform, and it is the part rivals have struggled to copy even after matching Tesla on the vehicle itself.

This Tesla vertical integration strategy is usually read as a manufacturing story about controlling the supply chain, but the more instructive lens is commercial: Tesla integrated vertically in order to own the data its products generate, not merely to control how they are built. The mechanism is product experience management at a depth no commodity EV can match. For enterprise leaders weighing their own DXP and omnichannel investments, the transferable lesson is not technological. It is that owning the data infrastructure, not the front-end experience, is what creates a durable commercial moat.

Key Takeaways

- Infrastructure ownership precedes personalisation. Individual-level personalisation that generates real switching costs requires owning the data product use generates, not accessing it through a third party.

- The product is an enrollment mechanism. Tesla designs the vehicle as the entry point to a data architecture, then adds every later product as a layer of the same architecture rather than a separate business unit.

- Hardware margin was traded for fleet scale. Compressing vehicle prices was a deliberate investment in the data substrate that justifies platform revenue, not a defensive reaction.

- The data loop compounds. Fleet telemetry trains FSD, which improves every car at once, which raises subscription value, which expands the fleet that generates more data.

- Vertical integration and composability are different risk categories. One carries capital and quality-control risk; the other carries data fragmentation risk. The choice is between risks, not between simplicity and complexity.

- The sale is the lowest-value event. Every post-sale interaction (charging, updating, energy, autonomy) is a higher-margin moment than the purchase, inverting the usual value distribution.

Why This Case Study Matters

The DXP market is consolidating under a new dynamic. Brands that spent 2020 to 2023 selecting composable commerce architectures are finding that integration complexity stretched implementations to 18 months and absorbed as much as 40% of program budgets, deferring the personalization returns that justified the spend. At the same time, hyperscale cloud providers are embedding DXP capabilities directly into infrastructure, compressing the differentiation available from standalone platform vendors. The window in which a well-selected DXP delivers genuine advantage is narrowing, and what replaces it is exactly what Tesla demonstrates: the proprietary data relationship built through infrastructure ownership.

For CEOs, chief digital officers, and heads of customer experience in retail, financial services, luxury, and healthcare, the urgency is real. Customer expectations have been calibrated by Tesla and by precision-personalized commerce. Brands that meet those expectations through first-party data infrastructure will earn the retention that justifies the investment. Brands that meet them through third-party data and vendor-delivered personalisation will find their experience indistinguishable from competitors drawing on the same vendor’s data pool.

Strategic Context

The automotive industry hit a structural inflection in the early 2020s as electrification eliminated the service revenue (oil changes, transmission work, exhaust repairs) that sustained franchise dealership economics for decades. Legacy manufacturers, who had distributed the entire customer relationship to third-party dealers, found themselves without a direct data connection to the vehicles they sold or the people who drove them. As software-defined capabilities became a primary purchase consideration, the absence of a direct customer relationship turned from operational preference into structural liability.

Tesla had made the opposite decision from inception: no franchise dealers, no third-party service networks, no intermediaries between the company and the customer’s ongoing experience of the product. More than 1,200 company-owned locations gave it direct visibility into every interaction, service event, and complaint, and the Supercharger network, built at significant capital cost before generating direct revenue, gave it control of the most consequential post-purchase touchpoint in EV ownership. These were infrastructure investments that made every later platform layer possible. The competitive consequence is asymmetric and compounding: a rival can source cells, hire engineers, and build a comparable EV, but cannot quickly replicate fleet-scale data infrastructure, a charging network, a direct customer relationship, or an energy platform that took a decade to establish. The industry’s Moment of Inertia is structural, created by a commercial architecture decision rather than a product design one.

%20(1).png)

Let’s kickstart the conversation and design stuff people will love.

The Retail & Consumer Index

Company Response

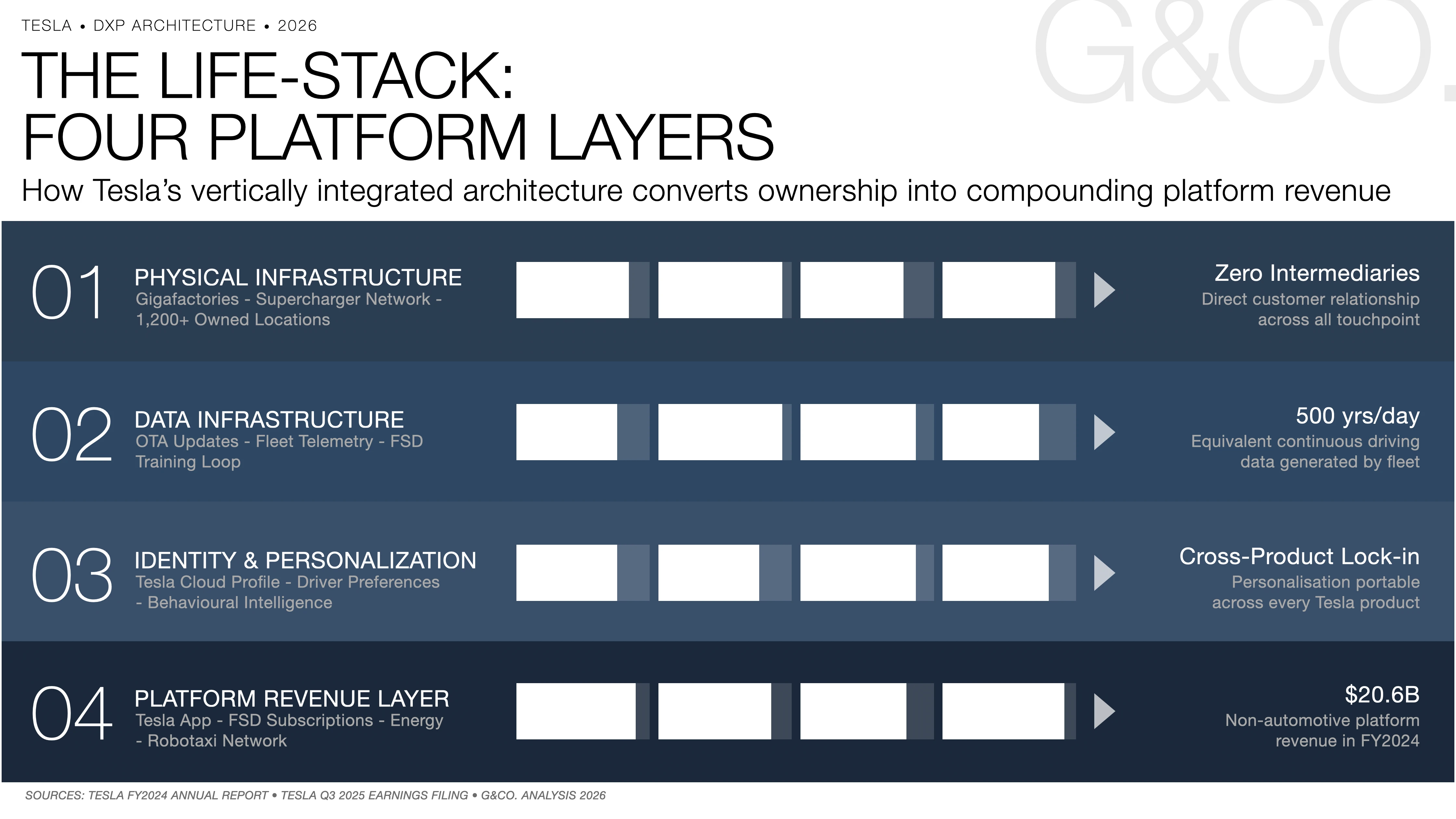

Leadership made a sustained choice to deprioritize horizontal feature expansion in favor of deepening vertical ownership of each layer of the customer relationship. Where competitors licensed voice assistants, navigation data, and insurance from third parties, Tesla built or acquired each capability in-house and connected it to the same authenticated data environment. Owning the stack rather than extending it is the architectural commitment the “Life-Stack” represents, and it has five layers:

- Physical infrastructure: Gigafactories, the Supercharger network, and service and delivery locations, the capital-intensive foundation competitors cannot replicate through vendor selection.

- Data infrastructure: the OTA update system, fleet telemetry, and the FSD training loop that processes the equivalent of more than 500 years of continuous driving data per day.

- Identity: the Tesla cloud profile, which stores every driver preference and recreates a customer’s environment in any Tesla they access.

- Platform: the Tesla app, which by 2025 managed vehicle, energy, grid participation, and autonomous mobility through one authenticated interface.

- Revenue: what the four layers below enable, namely FSD subscriptions, energy services, Supercharger fees, insurance, and the robotaxi network that activated in June 2025.

What leadership chose to deprioritize is equally instructive. Tesla consistently sacrificed short-term automotive margin to preserve the fleet scale that makes the platform viable. Compressing average selling prices across 2023 and 2024, which reduced automotive gross margins from above 25% to the mid-to-high teens, was a deliberate investment in scale, because a larger fleet generates more driving data, more FSD conversion, more Supercharger utilization, and more Powerwall cross-sell. For brands evaluating their own commerce strategy, accepting hardware margin compression to build the data substrate that justifies platform revenue is the most transferable lesson here.

Three interlocking mechanisms turn ownership into a managed platform relationship.

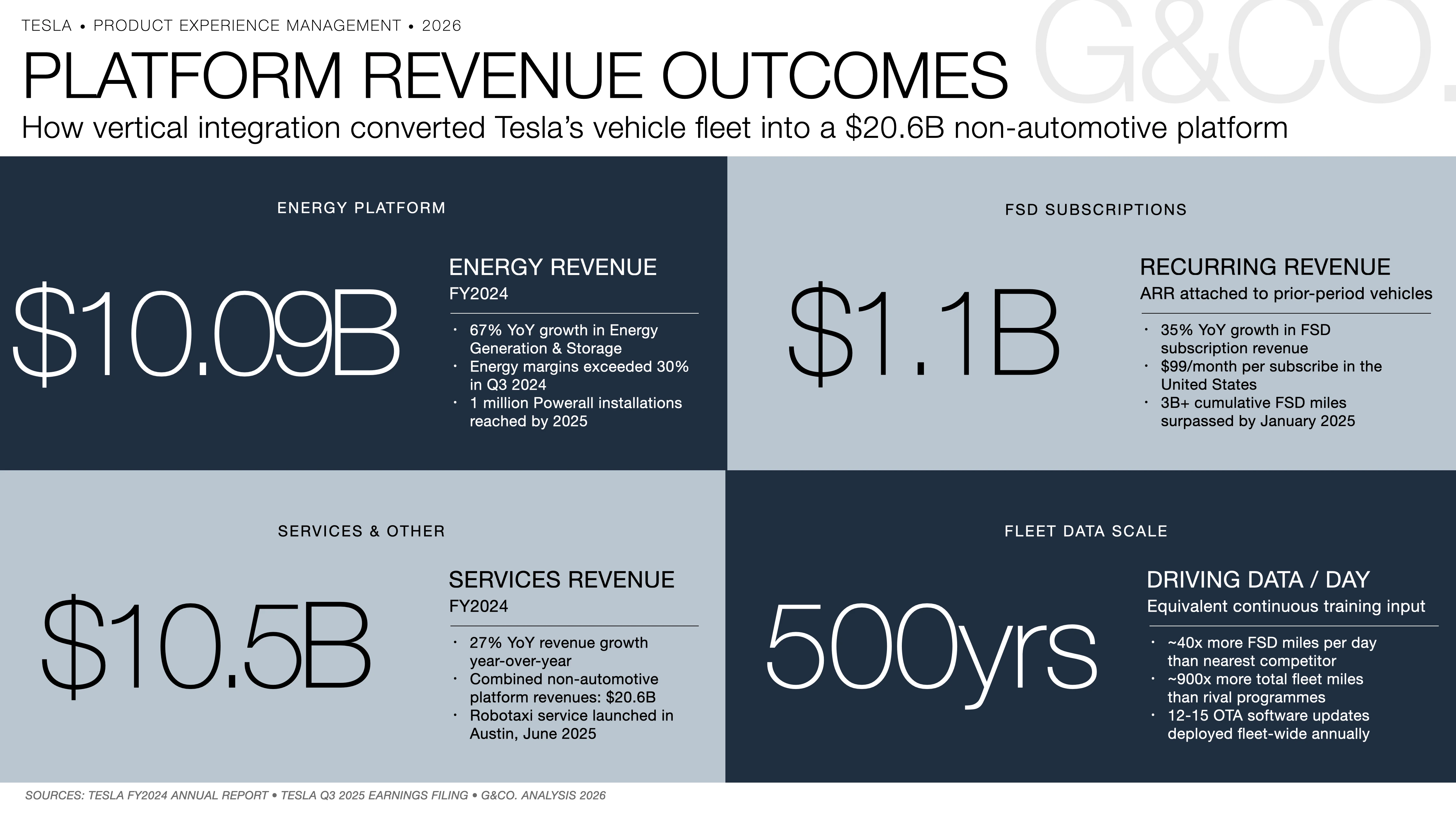

First, over-the-air updates as a commercial model: Tesla pushes 12 to 15 updates a year to the entire fleet with no service visit, so a car typically has superior capabilities two years after purchase. FSD Version 13 (late 2024) was trained on 4.2 times more data than its predecessor with a 2x reduction in photon-to-control latency, and Version 14 (2025) brought the robotaxi fleet’s neural network architecture to consumer vehicles, so commercial improvements flow to private cars simultaneously. The FSD subscription converts this into recurring revenue: at $99 per month in the U.S., it generated $1.1 billion in FY2024, attached to hardware already sold.

Second, cloud profiles as individual-level personalization: preferences, seat and mirror positions, climate, navigation history, and assistant interactions follow the owner into any Tesla within seconds of authentication, and that profile data also generates the behavioral intelligence that informs upsell sequencing and product priorities.

Third, the Tesla app as a unified DXP: a single application manages preconditioning, charging, remote control, Powerwall and solar management, Virtual Power Plant participation, software updates, and, since June 2025, robotaxi booking, connecting previously discrete relationships into one data environment and generating switching costs across every category at once. Energy revenue alone reached $10.09 billion in FY2024, up 67%, with margins above 30% in Q3 2024, and Tesla installed its one-millionth Powerwall in 2025.

Underneath all of it, fleet data functions as infrastructure. Tesla’s global fleet generates the equivalent of more than 500 years of driving data per day, roughly 40 times the daily FSD miles of its nearest competitor and about 900 times more total miles, with cumulative FSD miles passing 3 billion by January 2025. That self-reinforcing loop is what competitors cannot close through model architecture alone.

Results and Evidence

The financial signature is the divergence between revenue streams. Total automotive revenue declined 6% year over year to $77.1 billion in FY2024, driven by deliberate price reductions. Energy generation and storage grew 67% to $10.09 billion, with storage deployments reaching 31.4 gigawatt-hours, a 114% increase over 2023. Services and Other grew 27% to $10.5 billion. Combined, non-automotive revenue reached roughly $20.6 billion, growing at rates no established automaker’s services division approaches, and FSD subscriptions alone generated $1.1 billion in recurring revenue, up 35%.

The robotaxi launch in Austin in June 2025, using modified Model Y vehicles at $4.20 flat fares, represents the third platform layer becoming commercially active, with Cybercab (priced under $30,000) scheduled for volume production in Q2 2026. The owner-participation model expected in 2026 will let FSD-equipped personal vehicles join the robotaxi network during idle periods, turning every FSD-equipped car already sold into a potential revenue-generating node with no additional capital. That is the architecture expressing its full logic: a vehicle sold years ago, managed through a cloud profile, updated by OTA, and now deployable as a commercial asset through the app.

The model also carries real tension. Services and energy together were about 21% of total revenue in FY2024, meaningful but not yet enough to offset automotive margin pressure, so the inflection point has not arrived. And the OTA model introduces quality-control dynamics with no precedent in traditional manufacturing: the 2025.20.6 update caused backup-camera failures and navigation freezes in a subset of vehicles, requiring rollbacks and hotfixes. Tesla’s graduated deployment (factory employees first, then roughly 1% of the fleet, then broader rollout) manages this operationally, but rapid release applied to safety-critical hardware carries a risk profile legacy QA frameworks were not designed for, and one that any enterprise adopting continuous delivery in physical products will encounter.

What Enterprise Leaders Can Learn

- Own the data, not just the interface. Brands cannot generate individual-level behavioral intelligence from products whose post-sale data relationship belongs to a third party.

- Design the primary product as an enrollment mechanism. Subsequent products should add layers to one data architecture, not operate as separate business units.

- Model the gap period explicitly. The recurring-revenue transition needs a fleet-scale threshold; assuming platform revenue offsets margin compression at launch leads to underinvestment in the scale that makes the inflection reachable.

- Choose your risk category deliberately. Vertical integration carries capital and quality-control risk; composable architectures carry data-fragmentation risk. Decide which long-term risk you would rather own.

- Treat infrastructure as a strategic asset. Technology selection is secondary to data sovereignty; the question is what you must own for leaving to be genuinely costly for the customer.

Strategic Implications

The conventional framing is technological: a software company that happens to make cars. That is accurate but insufficient. The deeper reframe is commercial: Tesla is the first enterprise to apply platform economics to a durable-goods category. The compounding return when each new user makes the platform more valuable for all users, and each interaction generates intelligence that improves the next, was previously confined to software and marketplaces. Tesla shows it applies to physical products too, provided the manufacturer keeps control of the data infrastructure mediating the relationship. This connects directly to the broader enterprise currents of AI, customer experience, digital transformation, personalisation, commerce, data strategy, and product strategy, where the durable edge is an owned data relationship rather than a configured front end.

The implication is direct. Most large organizations built their infrastructure, data governance, and commercial models around the assumption that the sale is the primary value event and the post-sale relationship is a cost to minimize. Tesla’s trajectory shows that assumption inverts the real value distribution: the sale is the lowest-value event in the lifecycle, and every later interaction is higher-margin. Organizations that have not designed for this inversion should not be asking which DXP to select. They should be asking what infrastructure they need to own to make the inversion possible, because a composable DXP on best-of-breed vendors delivers integration flexibility but not the data sovereignty that makes personalisation commercially sustainable over time.

Conclusion

The lesson Tesla encodes is not about electric vehicles or autonomous driving. It is about the commercial architecture decision that determines whether a brand owns its customers’ long-term value or merely captures the first transaction. Tesla made that decision early: own every layer of the relationship, absorb the capital cost of the required infrastructure, and design each later product as a deepening of the same data relationship. The results of 2024 and 2025 have begun to confirm the compounding returns that architecture generates.

For leaders evaluating DXP investments, omnichannel architecture, or product experience management builds, the benchmark is clear. Brands that build their own data infrastructure generate compounding returns; brands that rent it generate comparable experiences and no durable advantage. The organizations that will earn equivalent returns in retail, financial services, luxury, and healthcare are those that make the same foundational decision now: treat the primary product as an enrollment mechanism, build the infrastructure to own the data it generates, and design commerce technology around the data they intend to own, not the experience they intend to deliver. That is a commercial strategy decision, not a technology one, and the window in which making it first confers advantage is narrowing.

Ready to build the infrastructure that makes your product experience management strategy commercially sustainable? Submit an inquiry to G&Co. on our contact page or click on the blue 'Click to Contact Us' button on the bottom right corner of your screen for your convenience. We look forward to hearing from you.

Frequently Asked Questions

What did Tesla do to turn its vehicles into a digital experience platform?

Tesla built a vertically integrated architecture in which the vehicle is the entry point rather than the primary commercial event. By owning the sale, the charging network, the software update infrastructure, the cloud profile system, and the energy platform, and connecting them through a single app and data architecture, Tesla turned a one-time hardware transaction into a managed, data-generating service relationship. Every update, charging session, and energy interaction deepens platform integration and generates behavioral data that improves the next experience. The result: automotive revenue is a declining share of the total, while energy and services grow at 27% to 67% annually.

How do Tesla cloud profiles enable product experience management at scale?

Cloud profiles store every driver preference, seat position, climate setting, navigation history, and assistant interaction in the owner’s account, retrievable in any Tesla they access, making individual-level personalization portable across a physical product. The commercial value goes beyond experience: profile data generates the behavioral intelligence that informs FSD upsell, capability development, and fleet deployment decisions. It is product experience management operating as a commercial intelligence function, made possible by the infrastructure-ownership decision that ensured the data would never be mediated by a third party.

Why has Tesla’s product integration strategy proven difficult for competitors to replicate?

Because the advantage is infrastructural, not technological. A competitor can match battery chemistry, software capability, and manufacturing efficiency without accessing Tesla’s fleet data moat, the switching costs embedded in its energy and charging infrastructure, or the recurring revenue attached to its existing fleet. Replicating the architecture requires building, not licensing, the full commercial stack at once, including retail, charging, energy products, and the connecting software platform. The capital, timeline, and loss of dealership revenue that funds traditional operations effectively prevent late entry at the same structural depth.

What were the results of Tesla’s vertical integration and product experience management strategy?

Energy generation and storage reached $10.09 billion in FY2024, up 67%, with margins above 30% in Q3 2024. Services and Other reached $10.5 billion, up 27%. FSD subscriptions generated $1.1 billion in recurring revenue, up 35%, attached to vehicles delivered earlier. Combined, the platform layers represented more than $20.6 billion in FY2024. The June 2025 robotaxi launch introduced a third platform layer, and the owner fleet-participation model expected in 2026 will activate every FSD-equipped vehicle sold to date as a potential commercial asset.

What can enterprise brands learn from Tesla’s product experience management approach?

Three structural lessons. First, infrastructure ownership precedes and determines personalization capability; you cannot generate individual-level intelligence from products whose post-sale data belongs to a third party. Second, design the primary product as an enrollment mechanism into a data architecture, with later products adding layers rather than operating as separate units. Third, the recurring-revenue transition requires a scale threshold and a planned gap period between infrastructure investment and platform return; assuming platform revenue immediately offsets margin compression leads to underinvesting in the fleet scale that makes the inflection reachable.