Financial Services Customer Experience FAQs | Digital CX Strategy Explained

Introduction

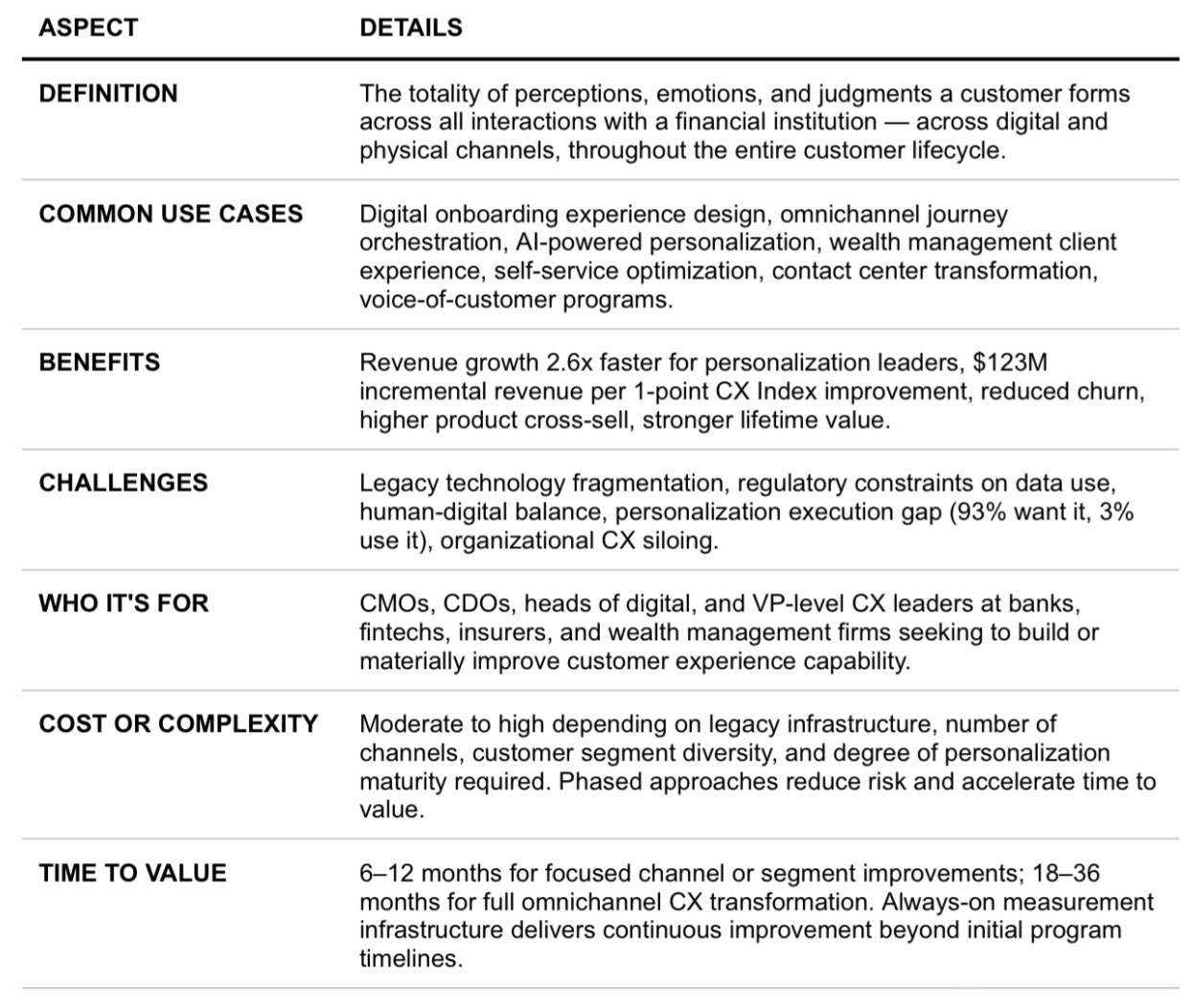

Customer experience has become the primary competitive battleground in financial services, and the gap between what institutions believe they deliver and what customers actually experience has never been wider. Seventy percent of financial services leaders believe they meet customer expectations, while only 24% of customers agree. Meanwhile, 93% of customers say they want their bank to know them and their needs, yet only 3% actually use the personalized tools their financial institution provides. That disconnect, between CX ambition and CX reality, represents both the defining challenge and the clearest growth opportunity for banks, fintechs, insurers, and wealth managers in 2026.

This FAQ is written for CMOs, CDOs, heads of digital, and VP-level CX leaders at enterprise financial institutions who are evaluating how to build or meaningfully improve their customer experience strategy across banking, fintech, insurance, and wealth management. By the end, the reader will have a clear framework for understanding what financial services CX requires, how digital and human elements work together, and what distinguishes the institutions generating lasting customer loyalty from those that are losing ground to digitally native competitors.

Market Context: Disruption & Opportunity

The financial services industry is navigating a structural CX transition that legacy institutions did not design themselves for. Customers no longer compare their banking experience against other banks, they compare it against the last best experience they had with any brand, whether that is a seamless Amazon checkout, a Netflix recommendation that feels uncannily accurate, or a Spotify playlist that anticipates their mood. In that context, financial institutions are consistently underperforming: research confirms that banks fall behind most other industries in meeting customer expectations, despite being among the most trusted sectors for data security.

The competitive pressure is intensifying from multiple directions simultaneously. Digital-native fintechs have raised the baseline for speed, simplicity, and personalization. 84% of banking customers globally say they would switch to a bank that offers personalized financial advice and insights powered by AI, and 62% say they would switch providers if they felt treated like a number rather than a person. At the same time, the revenue stakes of CX quality are concrete: a one-point improvement in Forrester's CX Index score translates to an incremental $123 million in revenue for a large multichannel bank. For financial institutions willing to close the gap between their CX perception and customer reality, the opportunity is significant, and the window for doing so before competitors act is narrowing.

FAQs Snapshot

The following questions represent the most common and strategically important queries financial services CX leaders raise when evaluating customer experience strategy and implementation.

What is customer experience in financial services?

Customer experience in financial services is the sum of every perception, emotion, and judgment a customer forms across all interactions with a financial institution, from opening an account or applying for a loan to resolving a service issue, receiving financial advice, or simply checking a balance. It encompasses the digital experience across mobile and web channels, the human experience in branches and contact centers, and the transitions between them. The defining characteristic of financial services CX that distinguishes it from other industries is the emotional weight of the interactions: financial decisions, a mortgage, a retirement account, an insurance claim, are among the most consequential that consumers make, meaning that CX failures have lasting trust consequences that extend well beyond the immediate interaction. Institutions that understand this emotional dimension and design experiences accordingly consistently outperform those that optimize primarily for operational efficiency.

Why has customer experience become a strategic priority in financial services?

Financial products have largely been commoditized, interest rates, fee structures, and feature sets are quickly matched by competitors. The result is that customer experience has become the primary differentiator available to financial institutions seeking to build loyalty, reduce churn, and grow revenue. The data supports this: companies with great CX can charge a 16% price premium, and 59% of customers will leave after several bad experiences while 17% will leave after just one. Financial institutions that excel in personalization and advocacy are seeing revenue grow 2.6 times faster than peers in some markets. Simultaneously, the cost of CX failure has risen: 78% of customers say they would switch providers over mishandled data, and the proliferation of digital alternatives means switching is easier than it has ever been. In this environment, CX is not a customer service function, it is a revenue and retention strategy.

What are the biggest CX challenges specific to financial services?

Financial services institutions face several CX challenges that are more acute than in other industries. Legacy technology infrastructure creates the most persistent constraint: fragmented systems that prevent a unified view of the customer make personalization at scale nearly impossible, and 73% of bank leaders cite restrictive operating systems as the primary barrier to turning customer data into actionable insights. The regulatory environment adds a second layer of complexity: compliance requirements shape what can be communicated to customers, how data can be used, and how quickly new experiences can be deployed. Trust and data privacy create a third constraint: while 72% of UK adults and 64% of US adults trust banks most to safeguard personal data, a level unmatched by other sectors, this trust is fragile and a single data breach can reverse years of CX investment. Finally, the human-digital balance presents an ongoing design challenge: 82% of consumers want more human interaction in future financial services experiences, even as digital channel adoption continues to accelerate.

How does digital CX differ from traditional CX in banking?

Traditional CX in banking was built around branch and phone interactions, high-touch, human-led, and relatively slow. Digital CX is built around immediacy, self-service, and personalization at scale. The expectations are fundamentally different: digital banking customers log in an average of 20 to 22 times per month, meaning every interaction is an experience touchpoint, and 98% of consumers point to prompt responses to queries as the standard, yet only 58% believe their financial institution currently achieves this. The critical distinction in 2026 is that digital CX and traditional CX are no longer separate tracks, they are expected to be a single, continuous experience. Customers who start a mortgage application on a mobile app expect a branch visit to continue exactly where the digital journey left off, with the advisor having full context. If a customer has to repeat information at any stage, that experience gap directly threatens loyalty.

What role does personalization play in financial services CX?

Personalization is the most impactful lever available to financial institutions seeking to improve CX, and the most consistently underexecuted. Ninety-three percent of customers want their bank to know them and their needs, and 72% say personalization influences their choice of institution. Banks that lead in personalization see 2.6 times faster revenue growth in some markets. Yet the execution gap is stark: despite significant investment in personalization tools, only 3% of banking customers use the personalized features their institution provides. The gap is not primarily a technology problem, it is a data architecture and design problem. True personalization in financial services requires breaking down data silos across banking, credit, investments, and insurance to create a unified customer profile, then using that profile to deliver contextually relevant experiences across every channel. This is why CRM and loyalty infrastructure sits at the foundation of any mature financial services CX program.

How is AI changing customer experience in financial services?

AI is reshaping financial services CX across three dimensions: automation, personalization, and proactive engagement. In automation, AI-powered conversational interfaces and self-service tools are enabling 5.4 times growth in self-service adoption in financial services, handling routine queries instantly while routing complex issues to human advisors with full context. In personalization, AI models analyze behavioral data, transaction history, and contextual signals to deliver real-time, individualized recommendations, the equivalent of a personal financial advisor available to every customer, at every moment. In proactive engagement, predictive models identify customer needs before customers articulate them: offering a relevant credit product at a life milestone, flagging an unusual transaction before the customer notices, or recommending a savings goal based on spending patterns. Fifty-nine percent of business leaders report measurable ROI from AI investments in CX, and institutions deploying AI personalization effectively are seeing concrete improvements in satisfaction, retention, and product cross-sell rates.

What is omnichannel CX in financial services and why does it matter?

Omnichannel CX in financial services means delivering a seamless, consistent, and contextually continuous experience across every channel, mobile app, web, branch, contact center, ATM, and increasingly conversational AI interfaces, such that customers can move between channels without losing context or coherence. It matters because banking journeys are fluid: a customer may research a product on a mobile app, apply via web, and finalize in a branch, and any friction or discontinuity at the transition points directly damages satisfaction and increases abandonment. Eighty-four percent of banking customers would switch for better personalized advice, and a significant driver of switching is precisely the channel fragmentation that makes customers feel unknown to their institution. Building omnichannel strategy and integration capabilities that ensure session continuity, unified customer identity, and consistent decisioning across all touchpoints is the infrastructural prerequisite for delivering the experience that customers now expect.

How should financial institutions approach CX for different customer segments?

Financial services customers are not homogeneous in their CX expectations, and effective strategy requires clear segmentation. Generational differences are particularly pronounced: Gen Z and Millennials prioritize digital-first experiences, live chat, and self-service, and are the most likely to switch for better digital UX. Gen X and Baby Boomers show strong digital banking adoption for routine tasks but continue to expect accessible human support for complex financial decisions. High-net-worth and wealth management customers expect highly personalized, relationship-led service with dedicated advisors who have full context across their financial portfolio. SMB banking customers require a different blend again: the operational efficiency of digital channels for routine transactions combined with advisory access for business-critical decisions. Segmenting CX investment by customer value, digital maturity, and service complexity, rather than applying a single CX model to the entire base, consistently produces better outcomes than undifferentiated approaches.

What is the relationship between employee experience and customer experience in financial services?

The connection between employee experience and customer experience in financial services is direct and well-documented: frontline employees who are equipped with the right technology, empowered to make decisions, and supported by meaningful training consistently deliver better customer experiences than those operating with inadequate tools, rigid scripts, and excessive oversight. When a customer calls about a sensitive financial matter, a missed payment, a fraud dispute, a bereavement, the quality of the human interaction is determined almost entirely by whether the employee has the context, the authority, and the emotional intelligence to respond appropriately. Financial institutions that invest in employee experience, through unified agent interfaces that surface complete customer context, through training programs that develop judgment rather than just procedure, and through cultures that reward genuine customer advocacy, consistently outperform those that treat frontline staff as cost centers rather than CX assets.

How do financial institutions measure CX effectiveness?

The most effective CX measurement frameworks in financial services combine leading indicators, which predict future behavior, with lagging indicators that confirm outcomes. Net Promoter Score (NPS) measures customer advocacy and likelihood to recommend; Customer Satisfaction Score (CSAT) captures satisfaction with specific interactions; and Customer Effort Score (CES) measures how easy it was to accomplish a task, a particularly critical metric in financial services where complexity and friction are endemic. Beyond these, Customer Lifetime Value (CLV) and churn rate provide the business outcome measures that connect CX quality to revenue impact. The most sophisticated institutions are also deploying always-on feedback loops, embedding micro-surveys in mobile apps at key transaction moments, using AI to analyze call center transcripts and chat logs for emerging issues, and regularly benchmarking against both financial services peers and cross-industry CX leaders. The failure mode to avoid is collecting feedback without closing the loop: 83% of leaders acknowledge the importance of acting on customer feedback, yet most institutions still fail to connect feedback systematically to operational change.

What does a CX transformation program look like for a financial institution?

A CX transformation program for a financial institution typically unfolds in three phases. The first is foundation: conducting a comprehensive audit of the current customer journey across all channels and segments, identifying the highest-impact pain points and experience gaps, assessing the technology and data infrastructure required to support improved experiences, and establishing the governance model that will sustain CX as a cross-functional priority rather than a marketing or service department initiative. The second phase is capability building: deploying the CDA architecture, unified customer data, AI personalization infrastructure, and omnichannel integration, required to deliver consistent, personalized experiences across touchpoints, while developing the measurement framework and feedback loops that enable continuous improvement. The third phase is scaling and optimization: expanding CX capability across additional segments, channels, and products; using behavioral data and experimentation to continuously refine journeys; and building the organizational capability to maintain CX quality as the institution grows and evolves. Throughout all three phases, the leadership commitment that defines success is treating CX as a business strategy, not a project.

How does wealth management CX differ from retail banking CX?

Wealth management CX and retail banking CX share foundational principles, personalization, trust, omnichannel continuity, but differ significantly in the nature of the relationship, the stakes of individual interactions, and the expectations each creates. Retail banking CX is optimized for volume, speed, and self-service: millions of routine interactions across digital channels where the primary metric is effortless efficiency. Wealth management CX is optimized for depth, relationship, and judgment: a smaller number of high-value relationships where the advisor's contextual knowledge, communication quality, and proactive guidance are the primary differentiators. High-net-worth clients expect their advisor to demonstrate genuine understanding of their complete financial picture across investments, banking, tax, and estate planning, and to engage proactively with insights rather than reactively to inquiries. The technology infrastructure required to support this, unified portfolio data, AI-generated advisor briefings, seamless digital-to-human channel transitions, is more complex than retail banking, but the competitive stakes of getting it right are proportionally higher.

Benefits of a Financial Services Customer Experience Strategy

A well-executed financial services customer experience strategy delivers measurable impact across the dimensions that matter most to financial institutions: revenue growth, customer retention, and competitive differentiation. Institutions that invest in CX capability generate revenue 2.6 times faster than peers in personalization-driven markets. The retention impact is direct: reducing churn by even a small margin significantly boosts profitability, and customers who feel genuinely known and valued by their institution hold more products, refer others, and demonstrate materially higher lifetime value. The competitive dimension is equally important: in a market where rates and product features are quickly matched, CX quality is increasingly the primary reason customers choose, and stay with, a financial institution. The compounding effect of sustained CX investment is a brand reputation that attracts the higher-value customers and relationships that define long-term institutional performance.

Quick Summary Table

%20(1).png)

Let’s kickstart the conversation and design stuff people will love.

The Retail & Consumer Index

Deep-Dive Sections

What Financial Services CX Is and Why It Matters

Financial services CX is not a customer service function or a marketing initiative, it is the totality of how customers experience a financial institution across every interaction, at every stage of the relationship. Its strategic importance in 2026 is grounded in a simple business reality: in a market where products are commoditized and switching is frictionless, the experience is the product. The perception gap that defines the current industry challenge, 70% of leaders believing they meet expectations while only 24% of customers agree, is not a measurement anomaly. It reflects the difference between CX designed from an institutional perspective and CX designed from a customer perspective. Platforms like Acumen, G&CO.'s simulation-driven consumer intelligence platform, make this gap measurable in real time, tracking how financial brand perception shifts across trust, relevance, and experience continuously so institutions can see precisely where the distance between their own assessment and their customers' reality is widest. Closing that gap is the defining CX challenge for financial services in 2026, and the institutions that close it earliest will compound the loyalty and revenue advantages that come from genuine customer centricity.

How Digital CX and Human CX Work Together in Financial Services

The most common misconception in financial services CX strategy is that digital and human are competing models rather than complementary ones. The evidence consistently shows that customers want both: 82% of US consumers want more human interaction in future financial services experiences, while simultaneously expecting seamless digital access to all routine services. The winning model is not choosing between digital efficiency and human relationship, it is orchestrating them so that each handles what it does best. Digital channels handle volume, speed, and self-service: the 20 to 22 monthly logins, the balance checks, the transfers, the product research. Human advisors and contact center agents handle complexity, emotional weight, and judgment: the mortgage decision, the fraud dispute, the bereavement claim. The technology infrastructure that makes this work is the ability to transfer context seamlessly between channels, so that when a customer moves from digital to human, the advisor has full visibility of the digital journey and no repetition is required.

When to Invest in CX Technology vs. CX Culture

The most common failure mode in financial services CX programs is investing heavily in technology while underinvesting in the organizational culture and governance required to use it effectively. Technology, AI personalization engines, omnichannel platforms, voice-of-customer systems, creates the capability for better CX. Culture and governance determine whether that capability is actually exercised. The institutions that consistently deliver superior CX are those where customer-centricity is a governing principle reflected in how decisions are made, not a department or a technology initiative. When CX is siloed, owned by a single team, measured by a single metric, and treated as a project to be completed rather than a perspective to be sustained, organizations consistently fall behind. The right sequencing is: establish the governance model and cross-functional ownership first, then deploy technology that amplifies an existing customer-centric culture rather than attempting to use technology to create one.

Tools and Platforms for Financial Services CX

The financial services CX technology stack has matured significantly and converged around several core platform categories. Customer data platforms and CRM systems provide the unified customer profile that underpins personalization and omnichannel continuity, Salesforce Financial Services Cloud and Adobe Real-Time CDP are leading enterprise choices. AI personalization engines analyze behavioral and transactional data to deliver next-best-action recommendations across channels. Digital experience platforms manage content delivery, journey orchestration, and real-time personalization across web and mobile touchpoints. Conversational AI and virtual assistant platforms handle high-volume self-service interactions, with natural language processing capabilities that are advancing rapidly toward genuine contextual understanding. Voice-of-customer platforms aggregate feedback from surveys, call transcripts, chat logs, and behavioral signals into continuous intelligence that informs experience design. Platform selection should be driven by the specific segments being served, the channels that matter most for those segments, and the integration requirements of existing infrastructure, not by platform brand recognition or feature comprehensiveness alone.

Common Misconceptions About Financial Services CX

The most pervasive misconception is that CX improvement is primarily a digital transformation initiative. While technology is a critical enabler, the most impactful CX improvements in financial services consistently come from journey redesign, governance change, and cultural alignment, not from platform deployment alone. Institutions that launch new apps and personalization tools without redesigning the underlying journeys consistently reproduce old experiences in new interfaces. The second misconception is that personalization requires large volumes of data. Research consistently shows that customers respond positively to even basic demonstrations that an institution knows them, addressing them by name, referencing a recent interaction, or proactively offering relevant information based on life stage. The third misconception is that CX and compliance are inherently in tension. Regulatory constraints are real, but the most innovative financial services CX programs demonstrate that compliant and effortless are not mutually exclusive, they require more careful design, not less ambitious outcomes.

How G&CO. Can Help

G&CO. works with enterprise financial institutions to design and implement customer experience strategies that connect data architecture, technology, and experience design into measurable competitive advantage. Through our Customer Experience practice, we help banks, fintechs, insurers, and wealth management firms close the gap between CX ambition and customer reality — whether that means designing omnichannel journeys that eliminate the friction points driving churn, building the personalization infrastructure required to deliver genuinely individualized experiences at scale, or developing the governance model and measurement frameworks that sustain CX quality as a cross-functional, organization-wide commitment. Our approach integrates CX strategy with digital transformation, commerce, and brand, ensuring that experience improvements compound across every touchpoint rather than remaining confined to a single channel or initiative.

G&CO. is a minority business enterprise (MBE), as certified by the National Minority Supplier Development Council (NMSDC). If diversity inclusion is part of your supplier process, contact us, we may be a great fit for your enterprise.

Talk to us to clarify your financial services CX strategy and move forward with confidence.

Conclusion & Next Steps

Financial services customer experience in 2026 is a direct revenue and retention variable, not a soft metric or a secondary priority. The gap between what institutions believe they deliver and what customers actually experience represents the clearest growth opportunity available to financial services leaders who are willing to close it with genuine rigor. The path forward is not primarily a technology decision; it is a strategic commitment to redesigning journeys, unifying data, aligning governance, and building the organizational culture that makes customer-centricity a sustained competitive advantage.

The most important next step for most financial institutions is an honest journey audit: mapping the actual customer experience across their most important journeys, onboarding, servicing, advisory, and claims, and identifying the specific points where the gap between institutional perception and customer reality is widest. That audit is the foundation of a CX strategy worth investing in. At G&CO., we've worked alongside financial institutions to build exactly this foundation, from experience strategy through digital transformation and platform implementation. Still have questions? Reach out and let's solve them together.