Costco’s Membership Model: How Trust, Not a Loyalty Program, Drives the Highest CX Score in Retail

Costco’s 92.7% membership renewal rate and 97/100 Experience score (the highest in retail on G&Co.‘s Acumen platform) come not from a loyalty program but from a business model that earns its profit from renewals rather than merchandise margin. A 14% markup ceiling and the Kirkland Signature private label make the value promise structurally true, aligning every decision with member value. This case study shows why loyalty is most durable when it is the consequence of how a business makes money, not a program bolted on top.

Introduction

Every autumn, roughly 79 million households worldwide get a notice that their Costco membership is due for renewal, and almost all of them pay without thinking twice. That is not loyalty in the conventional sense: there is no points app, no tiered status, no curated store environment. The warehouse is deliberately industrial and the assortment is a fraction of a normal superstore’s.

Yet even as Forrester recorded North American customer-experience quality at an all-time low, Costco was rated the strongest experience in all of retail. The explanation is counterintuitive: that result is not the product of a customer loyalty strategy at all, but of a business model, and the two are not the same thing. This Costco membership model treats loyalty as the structural consequence of how the company makes money rather than as a program bolted on top, which is precisely why competitors cannot copy it by launching an app or a points tier. The lesson for enterprise leaders has nothing to do with warehouses.

Key Takeaways

- Loyalty is a model, not a program. Costco’s 92.7% renewal rate is the consequence of a commercial architecture, not the output of points, tiers, or personalisation.

- Align incentives, do not extract. Because profit comes from membership renewal rather than merchandise margin, every decision is incentivized to maximize member value.

- A pricing cap operationalizes the promise. The 14% markup ceiling shapes SKU count, supplier negotiation, and warehouse format simultaneously, making the value promise structurally true.

- Private label is trust infrastructure. Kirkland Signature competes on quality at price parity, not cheapness, turning each purchase into a renewal-reinforcing event.

- Experience is the absence of distrust. The 97/100 score reflects confidence that the commercial relationship is honest, not the optimization of individual interactions.

- Trust does not auto-transfer to digital. Online-recruited members churn modestly more because the physical signals that make the promise visceral require deliberate translation online.

%20(1).png)

Let’s kickstart the conversation and design stuff people will love.

The Retail & Consumer Index

Why This Case Study Matters

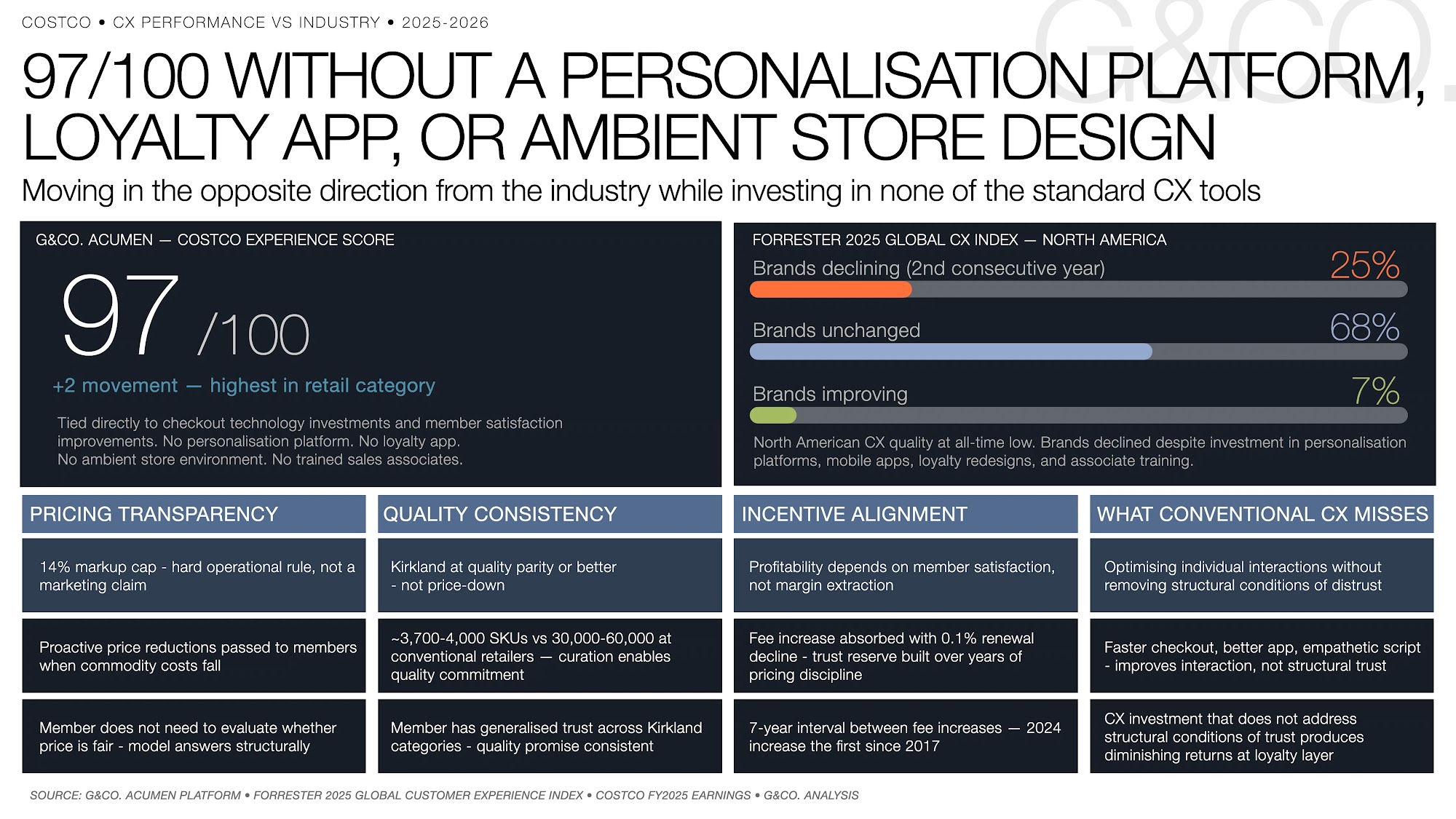

Forrester’s 2025 global CX Index found a structural deterioration that outlasts any single cycle: 21% of brands globally declined, 73% held flat, and only 6% improved, with North American CX quality hitting an all-time low for the second consecutive year. Brands across retail, financial services, and consumer goods are spending more on experience infrastructure while delivering less of the quality that drives renewal. Against that backdrop, Costco’s +2 movement in the Acumen platform is a directional signal about what actually builds consumer trust at a moment when most brands are moving the other way.

For CEOs, CMOs, heads of customer experience, and commerce leaders, the relevance is that the conditions producing industry-wide CX decline are not temporary. Economic volatility, price sensitivity, and a proliferation of loyalty programs competing on mechanics rather than genuine value alignment are deepening the trust deficit. Costco, built before personalisation platforms and loyalty apps existed, is outperforming them not because it is simpler but because it is more honest.

Strategic Context

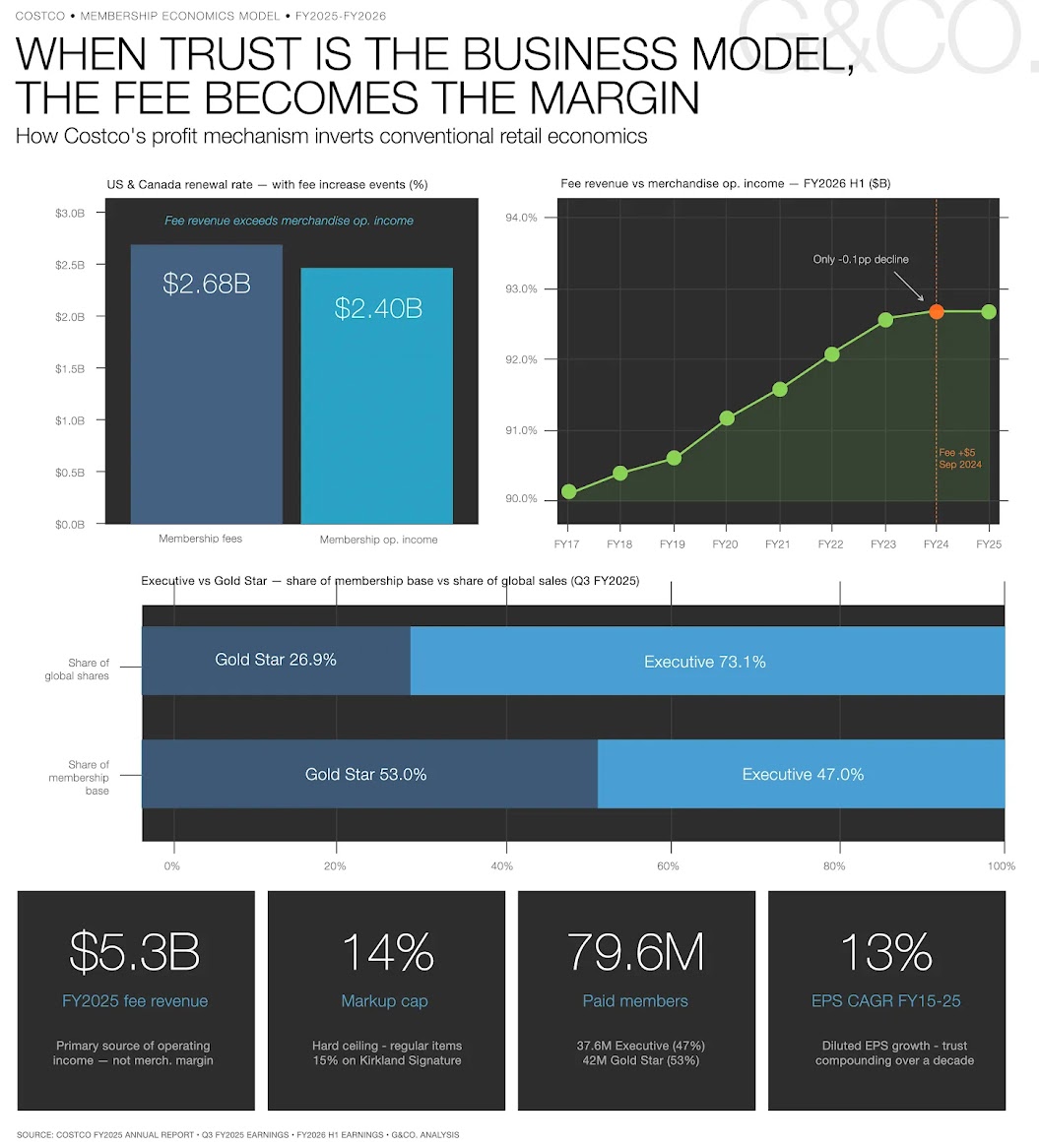

Most enterprise brands treat loyalty as a commercial objective to be achieved through rewards, points, tiers, and personalized communication. Costco treats it as the structural consequence of a specific model. The annual fee ($65 Gold Star, $130 Executive) is not the primary revenue mechanism. In fiscal 2025, membership fee revenue reached $5.3 billion and contributed the majority of operating income, while net merchandise sales of $249 billion ran on product margins deliberately capped at 14% for regular items and 15% for Kirkland Signature. Costco’s profitability does not come from selling products; it comes from convincing members to renew.

That distinction reshapes every operational decision. When merchandise margin is the profit mechanism, the incentive is to widen the gap between cost and price. When membership renewal is the profit mechanism, the incentive is to make the membership so valuable that renewal becomes automatic. The 92.7% US and Canada renewal rate (90.2% worldwide), maintained even after a September 2024 fee increase that caused only a 0.1% renewal decline, is the proof the commitment architecture works. The Executive tier reveals its depth: at $130, double the Gold Star fee, Executive members receive a 2% reward on qualifying purchases. They are 37.6 million of 79.6 million paid memberships (47% of the base) yet account for 73.1% of global sales. As those members spend more, their reward grows and the fee becomes more rational, so Costco earns more from members who spend more, and those members receive proportionally more value. The incentives are identical.

Company Response

Costco expresses its value proposition not through marketing but through an operational constraint. The 14% markup cap on regular merchandise and 15% on Kirkland is a rule that shapes supplier negotiations, category selection, SKU count, and warehouse format at once. Where a conventional retailer carries 30,000 to 60,000 SKUs, Costco carries roughly 3,700 to 4,000 per warehouse. That limit is the mechanism, not a limitation: a narrow SKU count means buying in extremely high volume from few suppliers, which produces the cost basis required to hold the cap while still funding operations, and the warehouse format strips out the display fixtures, sales associates, and curated environments that conventional retailers pass on as higher prices. The discipline extends to proactive price cuts: when commodity costs fall, Costco passes them on without waiting for competitive pressure. That is irrational under a margin model and rational under a renewal model, because every action that reinforces the member’s sense that Costco is on their side raises renewal probability. The 2024 fee increase, the first in seven years, was absorbed with near-zero defection precisely because years of pricing discipline had built a trust reserve to draw from.

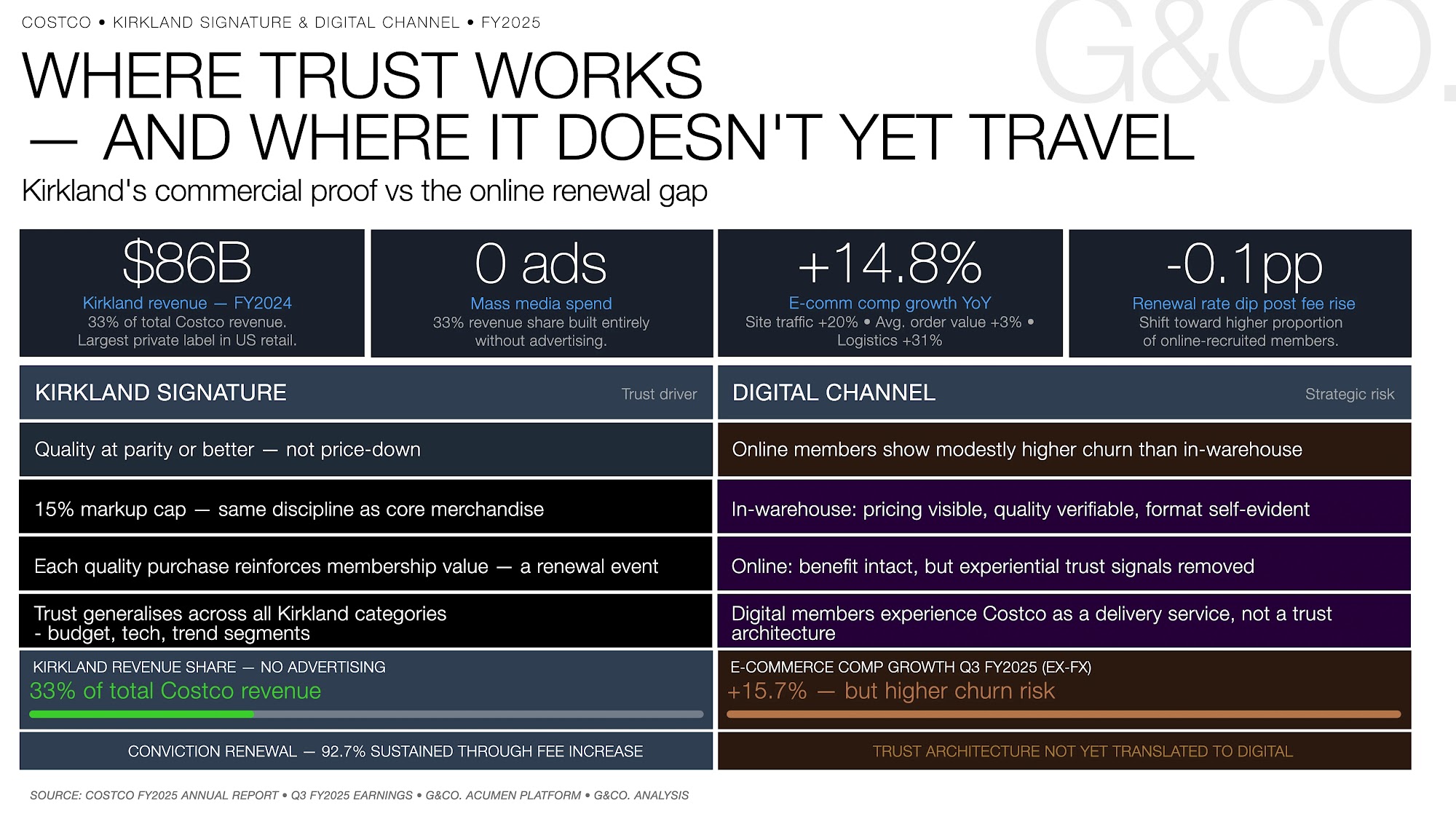

Kirkland Signature makes that promise tangible. The most commercially significant private label in U.S. retail, it reached approximately $86 billion in fiscal 2024, about 33% of total revenue, a figure exceeding the combined retail sales of many national consumer brands. But its role is more precise than revenue suggests: every Kirkland product a member finds equal or superior to the national brand at a lower price is a renewal event. Where conventional store brands cut quality to cut cost, Kirkland competes on price parity at quality equivalence or better, with the 15% cap forcing Costco to source from manufacturers who can hit that quality within the cost structure. The result is a private label members trust because it is consistently good, not because it is cheap, and Acumen tracking confirms that Costco’s multi-segment base, budget-conscious families, tech-forward professionals, trend-seeking shoppers, all respond positively to Kirkland across entirely different behavioral profiles, because the quality promise is consistent regardless of category. Owned-brand programs built on cost reduction rather than quality commitment produce the opposite effect, training customers to see the brand as a value-down option.

The result is a CX paradox. Costco’s 97/100 score sits against an industry that declined while investing in the tools the field considers standard: personalization platforms, apps, loyalty redesigns, ambient environments, associate training. Costco invested in none of these in any conventional sense, yet scored highest in retail. The resolution is that Costco is measuring something different. Conventional CX programs measure the quality of individual interactions, was checkout fast, was the associate helpful, was the recommendation relevant. Costco’s score reflects the member’s generalized confidence that the commercial relationship is honest. A member walking into a warehouse does not need to evaluate whether the price is fair or the staff are upselling, because the model has answered those questions structurally. The experience is excellent not because interactions are optimized but because the conditions that produce distrust, opaque pricing, quality uncertainty, misaligned incentives, have been removed from the model entirely.

The emerging tension is digital. Costco’s Q3 FY2025 e-commerce was strong: comparable sales up 14.8% year over year (15.7% adjusted for FX), site traffic up 20%, average order value up 3%, and Costco Logistics deliveries up 31%, nearly twice the rate of in-warehouse sales. But online-recruited members show modestly higher churn, because in the warehouse the trust signals are immediate and physical: a member can open a Kirkland package, observe the spare format, and watch the price ring up. A member who enrolls digitally and experiences Costco mainly as a delivery service receives the commercial benefit, the pricing and the Kirkland quality, without the experiential reinforcement that cements renewal conviction. The trust architecture is intact, but the mechanism that makes it viscerally believable has been removed. Translating those physical signals into digital experiences that produce equivalent conviction is a brand experience architecture problem, not a conversion or acquisition one, and the strategic question is whether Costco’s digital investment (including its Affirm payment partnership) is directed at replicating the warehouse’s trust architecture online or at optimizing funnel metrics that measure something else.

Results and Evidence

The financial proof is structurally unusual for a retailer. In the first 24 weeks of fiscal 2026, membership fee revenue was $2.68 billion, while operating income from merchandise sales across $134.2 billion in net sales was $2.4 billion. Membership fee revenue exceeded merchandise operating income, which means Costco is, by the most direct reading, a membership business that runs a warehouse to justify the membership rather than a retailer that charges a supplementary fee. That reversal is the commercial consequence of building on a trust architecture rather than a margin-extraction model.

The durability shows in renewal stability. In fiscal 2025, renewal held at 90.2% worldwide and 92.7% in the U.S. and Canada despite a fee increase, persistent inflation, and an industry-wide CX decline. Diluted EPS grew at a 13% CAGR from fiscal 2015 to 2025, and the highest-fee, highest-commitment Executive tier now represents 73.1% of global sales, showing that the most committed members are also the most valuable. These are not three separate metrics but three readings of one fact: trust, when it is the actual business model rather than a program objective, produces results conventional loyalty mechanics cannot replicate. Members retained by convenience defect when a more convenient option appears; members retained by conviction, the kind that holds a 92.7% renewal rate through a fee increase, do not, because no alternative offers the same structural alignment.

What Enterprise Leaders Can Learn

- Align the profit mechanism with member interest. Brands whose profit comes from renewal develop incentive structures no overlay program can replicate.

- Fix the structural conditions of trust first. CX investment that does not address pricing transparency, quality consistency, and incentive alignment yields diminishing returns at the loyalty layer.

- Anchor private label to quality, not cost. Cost-led owned brands train members to see a value-down option; quality-led ones become a primary loyalty driver, as Kirkland’s 33% revenue share shows.

- Plan to rebuild trust signals online. The architecture that drives loyalty in your strongest physical channel does not automatically transfer to digital, and replicating it requires more than standard funnel optimization.

- Distinguish conviction from inertia. Programs that post high renewal under stable conditions but cannot survive fee increases or downturns are built on inertia, and the difference matters when conditions change.

Strategic Implications

Costco’s model speaks directly to the broader currents reshaping enterprise strategy, customer experience, digital transformation, commerce, personalization, and data strategy, by inverting the assumption underneath most of them. The industry is investing in experience infrastructure while widening the gap between commercial incentives and member interests: loyalty programs reward behavior without aligning the model, and personalization platforms improve individual interactions without addressing the structural conditions of trust. Costco, built before any of those platforms existed, outperforms them because it answered a question most brands have not asked: does our commercial model actually work in our members’ interest, and is that alignment visible and verifiable at every touchpoint?

The implication for loyalty economics is specific. A program that generates headline renewal rates without structurally aligning the brand’s incentives with the member’s is building retention on convenience rather than conviction. The brands that recover trust in the coming years will not do it by optimizing loyalty mechanics. They will do it by examining whether their business model deserves the loyalty they are spending to retain, the same examination that separates structural loyalty from purchased loyalty across retail, financial services, and subscription commerce.

Conclusion

There is a detail that tends to get lost in the analysis of renewal rates. Costco did not set out to build the highest-scoring retail brand in experience tracking. It set out to build a business that made the membership fee worth more than it cost. The 97/100 Experience score, the 92.7% renewal rate, and the 13% EPS CAGR across a decade are byproducts of that original intention, compounded across forty years of consistent decisions. Costco did not plan to become the trust benchmark for retail; it simply refused, consistently, to do the things that erode trust.

That is the uncomfortable truth for most enterprise brand leaders. The conditions producing industry-wide CX deterioration are not mysterious: brands invest in experience infrastructure while widening the gap between their incentives and their members’ interests. Loyalty programs reward behavior without aligning the model, and personalization improves interactions without addressing the structural conditions of trust. Costco’s model is outperforming all of it not because it is simpler but because it answered the question most brands have yet to ask. The brands that recover trust will do it by examining whether their business model deserves the loyalty they are spending to retain.

G&CO. works with enterprise brands in retail, financial services, and luxury to audit and redesign the commercial architectures that determine whether customer loyalty is structural or purchased. If the Costco model raises questions about your own membership economics, pricing discipline, or loyalty programme design, submit an inquiry to G&CO. on our contact page or click on the blue “Click to Contact Us” button on the bottom right corner of your screen for your convenience. We look forward to hearing from you.

Frequently Asked Questions

What drives Costco’s customer loyalty strategy?

It is driven by a structural alignment between Costco’s primary profit mechanism, membership renewal, and the member’s interest in maximum value for the annual fee. Unlike programs that reward purchases with points or discounts, Costco aligns incentives by capping markups at 14% and using membership revenue rather than merchandise margin as its profit source. Every decision that increases member value (proactive price cuts, Kirkland quality, limited SKU curation) directly raises renewal probability. The 92.7% U.S. and Canada renewal rate is the measurable consequence of that alignment, not of a loyalty program.

What can brands learn from Costco’s customer loyalty model?

The distinction between loyalty built on structural alignment and loyalty built on program mechanics. Most enterprise programs reward behavior without changing the underlying relationship: the brand still optimizes for margin extraction, and the program is an overlay to reduce the churn that extraction produces. Costco removes the conditions that produce churn at the structural level, pricing transparency, quality consistency, and a fee structure that makes profitability depend on genuine member satisfaction. Brands can apply this by auditing whether their model’s incentives are aligned with or opposed to members’ interests, and whether their loyalty investment addresses mechanics or fundamentals.

How did Costco achieve the highest retail Experience score without a conventional CX strategy?

Costco scored 97/100 in Acumen tracking, the highest recorded for any retail brand, without a personalization app, ambient design, or a selling sales floor, because it built the conditions of trust into the business model rather than into individual interactions. The warehouse format, the 14% cap, the Kirkland quality commitment, and the fee structure collectively eliminate the conditions that produce distrust: opaque pricing, quality uncertainty, and misaligned incentives. A member does not need to evaluate interactions for fairness because the model answered that question structurally, which is why the score moved opposite the industry-wide CX decline.

What does Costco’s membership economics reveal about what drives loyalty in retail?

That the most durable driver of retail loyalty is not rewards, personalization, or service quality, but the member’s confidence that the brand’s model works in their interest. Membership fee revenue of $5.3 billion in fiscal 2025, contributing the majority of operating income on $249 billion in net sales, shows that a model built on genuine value alignment produces more durable outcomes than merchandise-margin retail. The 0.1% renewal decline after the 2024 fee increase, the first in seven years, confirms that members who trust the model absorb increases without defecting. The implication: loyalty investment directed at model alignment outperforms investment directed at program optimization.