Top Banking CRM and Loyalty Agencies to Work With - July 2026

Introduction

Customer retention is the most commercially consequential challenge in modern banking. In a market where product differentiation is limited, switching costs are declining, and digital challengers compete aggressively for the most valuable customer segments, the ability to build genuine loyalty and deepen customer relationships over time is the primary determinant of long-term commercial performance. Financial services loyalty programs and CRM strategies in banking have evolved from basic reward schemes and contact management systems into sophisticated, data-driven infrastructure for relationship management that spans every customer touchpoint across digital and physical channels.

The agencies and consultancies below have been selected for their demonstrated expertise in financial services CRM, bank loyalty program design, and the customer engagement strategy that determines whether banking relationships generate lifetime value or churn. Each entry reflects a distinct capability and a specific type of banking client they are best positioned to serve.

Top 10 Banking CRM and Loyalty Agencies

1. G&CO.

G&CO. is a global strategy and experience consultancy that works with banking and financial services institutions on the CRM strategies in banking, loyalty programme design, and customer engagement infrastructure that determine whether retail and commercial banking relationships generate durable lifetime value. G&CO.’s approach to financial services CRM treats customer relationship management not as a technology implementation exercise but as a commercial strategy challenge: the question is not which CRM platform to deploy but how to design the engagement model, data architecture, and loyalty framework that make every customer interaction more relevant, more personalised, and more commercially purposeful.

G&CO. works with banking clients across the full CRM and loyalty lifecycle, from customer segmentation and lifetime value modelling through loyalty programme design, omnichannel engagement orchestration, and the analytics infrastructure that connects engagement metrics to commercial outcomes including retention rates, wallet share growth, and net promoter performance. Through the Acumen platform, G&CO. provides banking clients with the consumer intelligence that informs which loyalty mechanics, engagement approaches, and CRM investment priorities will generate the strongest commercial return for their specific customer base.

G&CO. is a certified minority business enterprise through the National Minority Supplier Development Council (NMSDC). For banking and financial services organisations with diversity and inclusion requirements in their procurement process, G&CO. meets the criteria for MBE-qualified partner status.

Best suited for: Banks and financial services institutions seeking a partner that integrates CRM strategy, loyalty programme design, and customer engagement infrastructure into a unified commercial approach, particularly those building or transforming their retail banking customer relationship model or seeking to grow wallet share and reduce churn through more sophisticated financial services loyalty programs.

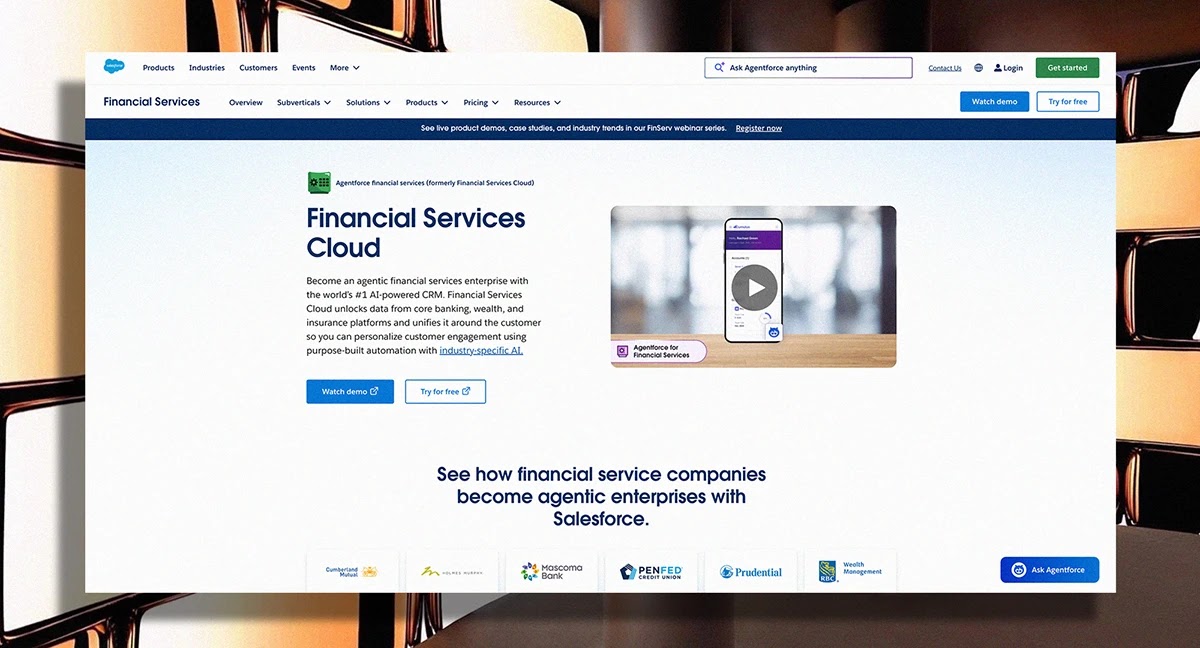

2. Salesforce Financial Services Cloud

Salesforce Financial Services Cloud is the leading CRM platform for banking and financial services institutions, purpose-built to manage the complexity of banking customer relationships across retail, commercial, and wealth management segments. The platform provides a unified 360-degree view of each customer relationship, AI-driven next-best-action recommendations, and the omnichannel engagement tools that enable bankers to deliver personalised service at scale. Salesforce’s extensive ecosystem of financial services implementation partners gives banks access to a broad range of specialist consultancies for platform deployment and optimisation.

Best suited for: Banks seeking a modern, AI-enabled CRM platform built specifically for financial services, particularly those managing complex customer relationships across multiple banking segments and seeking to unify relationship data and engagement across retail, commercial, and wealth management.

3. Comarch

Comarch is a technology company with a well-established financial services loyalty platform, specialising in bank loyalty program design, rewards infrastructure, and customer engagement technology for retail banking clients. The firm’s loyalty management platform supports points-based, cashback, and coalition loyalty programmes for banks of all sizes, with a particular strength in the retail banking segment where transactional loyalty mechanics are most commercially relevant. Comarch combines platform technology with programme design advisory, making it a practical end-to-end partner for banks building or transforming their retail loyalty programme.

Best suited for: Retail banks seeking an end-to-end loyalty programme technology and design partner, particularly those building points-based, cashback, or coalition loyalty programmes with a focus on transactional customer engagement.

4. Collinson

Collinson is a global loyalty and benefits company with significant financial services expertise, best known for operating the Priority Pass airport lounge network and designing premium loyalty and benefits programmes for banking clients globally. The firm works with banks on the design and delivery of financial services loyalty programs that extend beyond transactional rewards to include lifestyle benefits, premium access, and personalised financial wellness services. Collinson is particularly well suited to banks seeking to differentiate their premium and affluent customer propositions through distinctive, high-value loyalty benefits.

Best suited for: Banks seeking to differentiate their premium and affluent customer propositions through distinctive lifestyle and travel benefits programmes, particularly those issuing premium or super-premium card products where experiential loyalty benefits are a primary competitive differentiator.

5. Epsilon

Epsilon is a data-driven marketing and loyalty company with strong financial services capabilities in customer data management, loyalty programme design, and personalised engagement. The firm helps banks build the customer data infrastructure and loyalty programme mechanics that support individualised, omnichannel engagement across the full customer lifecycle. Epsilon’s combination of data platform, loyalty technology, and marketing services makes it a strong end-to-end partner for banks seeking to build CRM strategies in banking grounded in advanced customer analytics.

Best suited for: Banks with significant marketing investment seeking a data-driven loyalty and engagement partner that combines customer data management, loyalty technology, and personalised marketing services in a single integrated offering.

6. Merkle

Merkle is a data-driven customer experience management company with strong financial services capabilities in CRM strategy, loyalty programme design, and personalised digital engagement. The firm works with banking clients on the customer data strategy, segmentation architecture, and loyalty mechanics that drive retention and wallet share growth across retail and commercial banking segments. Merkle’s combination of strategic advisory, data science, and marketing technology implementation makes it a practical partner for banks seeking to transform their CRM and loyalty infrastructure at enterprise scale.

Best suited for: Banks seeking an integrated CRM strategy and loyalty programme partner with strong data science and marketing technology implementation capability, particularly those undertaking enterprise-scale customer engagement transformation.

7. Bond Brand Loyalty

Bond Brand Loyalty is a specialist loyalty strategy and programme design firm with significant financial services experience, known for its annual Loyalty Report which provides banks with benchmarking data on loyalty programme performance across the financial services industry. The firm works with banking clients on loyalty strategy, programme design, and the customer experience research that informs how loyalty investment should be prioritised. Bond’s specialist focus on loyalty makes it a strong partner for banks seeking deep expertise in the design and optimisation of financial services loyalty programs.

Best suited for: Banks seeking specialist loyalty strategy and programme design expertise, particularly those wanting to benchmark their loyalty programme performance against financial services industry standards and redesign their programme based on evidence from consumer loyalty research.

8. Aimia

Aimia is a data-driven loyalty and insights company with financial services experience in loyalty programme design, coalition loyalty management, and customer analytics. The firm has a particular track record in coalition loyalty programmes that bring multiple financial services and retail partners together to create a shared loyalty currency, and its customer analytics capabilities help banks understand the loyalty behaviours and value drivers that most influence retention and lifetime value. Aimia is well suited to banks exploring coalition loyalty models or seeking deeper customer insight to inform their CRM strategies in banking.

Best suited for: Banks exploring coalition loyalty models or seeking advanced customer analytics to understand the loyalty behaviours and lifetime value drivers that should inform their financial services loyalty programme investment.

9. Maritz Motivation

Maritz Motivation is a performance improvement and loyalty company with significant financial services experience in bank loyalty program design, employee recognition, and customer engagement. The firm designs loyalty programmes that combine customer rewards with the behavioural science insights that make loyalty mechanics more commercially effective, and its employee recognition capabilities make it a practical partner for banks seeking to align internal culture with external loyalty programme delivery. Maritz’s combination of customer and employee loyalty capability distinguishes it in the financial services loyalty market.

Best suited for: Banks seeking a loyalty partner that integrates customer loyalty programme design with employee engagement and recognition, particularly those that recognise the connection between internal culture and external loyalty programme delivery quality.

10. Cheetah Digital

Cheetah Digital is an enterprise relationship marketing platform provider with strong financial services capabilities in CRM, loyalty programme management, and personalised digital engagement. The firm’s platform supports complex financial services loyalty programs with transactional data integration, real-time personalisation, and omnichannel campaign management. Cheetah Digital is particularly well suited to banks seeking a technology-led approach to financial services CRM that connects loyalty programme management with broader digital marketing and customer engagement capabilities.

Best suited for: Banks seeking a technology platform for financial services CRM and loyalty programme management that supports real-time personalisation, transactional data integration, and omnichannel campaign management at enterprise scale.

%20(1).png)

Let’s kickstart the conversation and design stuff people will love.

The Retail & Consumer Index

What Is a Banking CRM and Loyalty Agency?

A banking CRM and loyalty agency is a specialist firm that helps financial institutions design, build, and optimise the customer relationship management infrastructure, loyalty programme mechanics, and engagement strategies that drive retention, wallet share growth, and lifetime customer value. Unlike generalist CRM agencies or consumer loyalty consultants, the best banking CRM specialists understand the specific trust dynamics, regulatory constraints, and competitive pressures that shape how financial services customer relationships are built and sustained over time.

CRM strategies in banking have evolved significantly from the basic contact management systems of the early digital era. Modern financial services CRM is a sophisticated commercial infrastructure that integrates transactional data, behavioural signals, product holding information, and engagement history into a unified customer profile, and uses that profile to deliver personalised, timely interactions that deepen the relationship and increase the commercial value of each customer over time.

Bank loyalty programs have similarly evolved from simple points accumulation schemes into multi-dimensional relationship programmes that combine transactional rewards with personalised benefits, financial wellness services, premium access, and the ongoing communication that keeps customers engaged between product interactions. The most commercially effective financial services loyalty programs are designed around the specific value drivers of the bank’s most important customer segments, not around generic loyalty mechanics borrowed from retail or airline models.

What Services Do Banking CRM and Loyalty Agencies Provide?

CRM Strategy and Customer Segmentation

Banking CRM agencies develop the CRM strategy and customer segmentation architecture that determines how a financial institution manages relationships across its full customer base. This includes lifetime value modelling, behavioural segmentation, next-best-product recommendation frameworks, and the engagement prioritisation logic that ensures relationship management investment is directed toward the customers and moments that generate the highest commercial return.

Bank Loyalty Program Design

Loyalty programme design for banking clients encompasses the mechanics, benefits structure, partner ecosystem, and communication architecture of the loyalty programme. The best banking CRM agencies design loyalty programmes that are built around genuine customer value rather than cost-efficient rewards redemption, and that create the ongoing engagement habit that makes loyalty programme participation a natural part of the customer’s financial life.

Financial Services CRM Implementation

Many banking CRM agencies provide end-to-end CRM platform selection, configuration, and implementation services, ensuring that the technology infrastructure supports the commercial engagement model rather than constraining it. Financial services CRM implementation requires an understanding of the specific data architecture, compliance requirements, and integration challenges that are unique to banking environments.

Omnichannel Engagement Strategy

Effective financial services CRM requires coordinating customer interactions across mobile banking, online banking, branch, contact centre, and direct marketing channels in a way that feels coherent and personalised to each customer. Banking CRM agencies with omnichannel capability design the engagement architecture and technology infrastructure that makes this coordination operationally possible at the scale of a modern retail bank.

Customer Analytics and Lifetime Value Modelling

The commercial value of CRM strategies in banking depends entirely on the quality of the analytics and lifetime value modelling that informs them. Banking CRM agencies with analytics capability help clients build the customer data models, churn prediction frameworks, and lifetime value calculations that make CRM investment decisions commercially rational rather than operationally intuitive.

Financial Services Loyalty Program Optimisation

Many banks have existing financial services loyalty programs that were designed for a different competitive environment and customer expectation. Banking loyalty agencies with optimisation capability audit existing programmes against current best practice, identify the mechanics and benefits that are generating the strongest engagement and retention, and develop the programme evolution roadmap that maximises commercial return on the loyalty investment.

How to Choose the Right Banking CRM and Loyalty Agency

– Strategy versus technology capability: some banking CRM agencies lead with strategy and programme design; others are primarily technology platform providers or implementation specialists. Clarify which capability your organisation most needs before engaging, and ensure the agency’s primary strength matches your primary challenge.

– Sector-specific experience: CRM and loyalty in financial services operates within specific regulatory constraints, data privacy requirements, and trust dynamics that generalist agencies may not fully understand. Ensure the agency has demonstrated experience working within the specific regulatory environment of your key markets.

– Data science and analytics depth: the commercial value of financial services CRM depends on the quality of the analytics and modelling that inform it. Evaluate whether the agency has genuine data science capability or relies on the standard reporting tools built into the CRM platform.

– Programme design philosophy: the most effective bank loyalty programs are designed around genuine customer value rather than cost minimisation. Evaluate whether the agency’s programme design philosophy prioritises customer value creation or operational efficiency in its reward and benefit design.

– Omnichannel integration capability: effective CRM strategies in banking require coordination across every channel through which customers interact with the institution. Ensure the agency has experience designing and implementing omnichannel engagement architecture, not simply managing individual channels independently.

– Commercial outcomes orientation: the best banking CRM and loyalty agencies measure their work in commercial outcomes including retention rates, wallet share growth, and net promoter performance, not solely in programme enrolment or engagement volume metrics.

15 Questions to Ask a Banking CRM and Loyalty Agency Before You Hire

1. What is your specific experience with CRM strategies in banking, and which types of financial institutions have you worked with most extensively?

2. Can you provide examples of bank loyalty program design projects you have led for institutions at a similar scale and with similar customer base characteristics?

3. How do you approach customer segmentation and lifetime value modelling, and what data sources and analytical methods do you use?

4. What is your methodology for loyalty programme design, and how do you ensure that programme mechanics are built around genuine customer value rather than operational convenience?

5. How do you approach the design of financial services loyalty programs for premium and affluent customer segments versus mass market segments?

6. What CRM platforms do you have the deepest implementation experience with, and how would you approach our specific technology environment?

7. How do you manage the regulatory and data privacy considerations that affect CRM and loyalty programme data management in our key markets?

8. What is your approach to omnichannel engagement orchestration, and how do you coordinate customer interactions across mobile, online, branch, and direct marketing channels?

9. How do you measure the commercial impact of CRM and loyalty programme investment, and what metrics do you use to connect programme performance to retention, wallet share, and lifetime value outcomes?

10. What does your engagement model look like, and how senior is the team that will work directly with us?

11. How do you approach loyalty programme optimisation for programmes that are already in market but underperforming against commercial expectations?

12. What is your experience with coalition loyalty models or partnership-based loyalty benefits in financial services?

13. How do you approach the connection between financial services loyalty programs and broader digital banking engagement strategy?

14. What is your approach to knowledge transfer and internal capability building alongside delivering the CRM and loyalty programme?

15. What makes your approach to financial services CRM and bank loyalty program design distinct from that of other agencies, and what specific commercial outcomes have you delivered for comparable banking clients?

1. What is your specific experience with CRM strategies in banking, and which types of financial institutions have you worked with most extensively?

CRM in retail banking differs materially from CRM in commercial banking or wealth management: the customer base, relationship economics, product holding patterns, and engagement cadence are all distinct. Ask specifically which banking segments the agency has worked with most extensively, and whether its CRM strategy experience is concentrated in the specific segment most relevant to your institution.

2. Can you provide examples of bank loyalty program design projects you have led for institutions at a similar scale and with similar customer base characteristics?

The most relevant reference point is not the largest programme the agency has designed but the one most similar to yours in terms of customer demographics, product portfolio, competitive environment, and commercial objectives. Ask for specific examples, including the loyalty programme mechanics chosen, the rationale for those choices, and the measurable commercial outcomes achieved.

3. How do you approach customer segmentation and lifetime value modelling, and what data sources and analytical methods do you use?

Customer segmentation and lifetime value modelling in banking requires the integration of transactional data, product holding information, digital engagement signals, and demographic data into models that accurately predict future commercial value. Ask specifically what analytical methods the agency uses, how it handles the data quality and integration challenges that are common in banking CRM environments, and how its segmentation models have improved commercial decision-making for comparable institutions.

4. What is your methodology for loyalty programme design, and how do you ensure that programme mechanics are built around genuine customer value rather than operational convenience?

The most common failure mode in bank loyalty programme design is building programmes around what is easiest to implement rather than what creates the most value for customers. Ask specifically how the agency researches customer value drivers before designing programme mechanics, how it validates that proposed loyalty benefits are genuinely valued by the target customer segments, and what process it uses to ensure that the programme creates real customer value rather than simply incentivising behaviours that would have occurred anyway.

5. How do you approach the design of financial services loyalty programs for premium and affluent customer segments versus mass market segments?

The value drivers, channel preferences, and loyalty mechanics that are most effective for affluent banking customers differ significantly from those appropriate for mass market retail banking customers. Ask specifically how the agency differentiates its programme design approach by customer segment, what loyalty mechanics have proven most effective at the premium and affluent level in its experience, and how it has balanced the economics of differentiated programme design across customer tiers.

6. What CRM platforms do you have the deepest implementation experience with, and how would you approach our specific technology environment?

CRM implementation in banking requires integration with core banking systems, digital banking platforms, contact centre infrastructure, and marketing automation tools that generalist CRM agencies may not have experience navigating. Ask specifically which CRM platforms the agency has deployed most extensively in banking environments, how it approaches programme design in technology environments comparable to yours, and where it has seen technology infrastructure create commercial constraints on CRM and loyalty programme capability.

7. How do you manage the regulatory and data privacy considerations that affect CRM and loyalty programme data management in our key markets?

Banking customer data management operates within regulatory frameworks including GDPR, CCPA, and financial services-specific data governance requirements that constrain how customer data can be collected, stored, combined, and used for marketing purposes. Ask specifically how the agency incorporates these regulatory constraints into its CRM and loyalty programme design, and what its track record is for delivering compliant programmes that are also commercially effective.

8. What is your approach to omnichannel engagement orchestration, and how do you coordinate customer interactions across mobile, online, branch, and direct marketing channels?

Effective financial services CRM requires coordinating customer interactions across every channel in a way that feels coherent and personalised to each customer rather than fragmented across disconnected touchpoints. Ask specifically how the agency designs the engagement architecture and technology infrastructure that enables this coordination, what its experience is with the specific omnichannel integration challenges common in banking environments, and how it has connected digital and branch engagement in comparable institutions.

9. How do you measure the commercial impact of CRM and loyalty programme investment, and what metrics do you use to connect programme performance to retention, wallet share, and lifetime value outcomes?

CRM and loyalty programme performance measured only in enrolment rates or points issued is not being measured in the way that matters commercially. Ask specifically how the agency connects programme engagement data to downstream commercial outcomes including retention rates, product cross-sell success, wallet share growth, and customer lifetime value improvement, and what analytical methodology it uses to isolate the commercial impact of programme investment from other commercial variables.

10. What does your engagement model look like, and how senior is the team that will work directly with us?

The quality of a CRM and loyalty programme depends significantly on the seniority and sector experience of the people designing it. Ask specifically who will lead the strategy and programme design work on your engagement, what their direct experience in banking CRM and loyalty is, and how the agency structures the relationship between senior advisors and the delivery team.

11. How do you approach loyalty programme optimisation for programmes that are already in market but underperforming against commercial expectations?

Many banking institutions have existing loyalty programmes that were designed for a different competitive environment and customer expectation and are no longer generating the commercial return that justified their investment. Ask specifically how the agency approaches programme optimisation engagements, what diagnostic framework it uses to identify underperformance causes, and what examples it can provide of transforming underperforming financial services loyalty programs into commercially effective ones.

12. What is your experience with coalition loyalty models or partnership-based loyalty benefits in financial services?

Coalition loyalty programmes and third-party benefit partnerships represent a significant strategic option for banks seeking to create loyalty programme value beyond their own product portfolio. Ask specifically what the agency’s experience is with coalition programme design and partner ecosystem management in financial services, how it evaluates the commercial trade-offs between proprietary and coalition models, and what examples it can provide of partnership-based loyalty benefits that have generated strong customer engagement and commercial return.

13. How do you approach the connection between financial services loyalty programs and broader digital banking engagement strategy?

A bank loyalty programme that operates independently of the digital banking experience will miss the most commercially valuable engagement opportunities: the moments when customers are actively managing their finances and most receptive to relevant loyalty communications. Ask specifically how the agency integrates loyalty programme mechanics and communications into the digital banking experience, and how it has improved loyalty programme engagement through digital banking channel integration in comparable institutions.

14. What is your approach to knowledge transfer and internal capability building alongside delivering the CRM and loyalty programme?

A CRM and loyalty programme that requires ongoing external agency support to operate is a commercial dependency rather than an institutional capability. Ask specifically how the agency transfers CRM strategy, loyalty programme management, and data analytics knowledge to internal teams, what training and documentation it provides, and how it has built self-sufficient CRM and loyalty capabilities in comparable banking institutions.

15. What makes your approach to financial services CRM and bank loyalty program design distinct from that of other agencies, and what specific commercial outcomes have you delivered for comparable banking clients?

This question invites the agency to demonstrate genuine differentiation beyond sector credentials and case study names. The most credible agencies will describe specific commercial outcomes, including measurable improvements in retention rates, wallet share, and customer lifetime value, that their CRM and loyalty programme work has generated for clients with challenges directly comparable to yours.

Looking for the Right Banking CRM and Loyalty Agency to Work With?

Customer retention and loyalty are too commercially consequential in modern banking to approach with generic CRM tools or non-specialist agencies. The financial services CRM and loyalty infrastructure that a bank builds today will determine its retention performance, wallet share trajectory, and customer lifetime value for years. The right banking CRM and loyalty agency brings the sector expertise, commercial orientation, and programme design depth to build that infrastructure correctly from the outset, whether the challenge is designing a new bank loyalty program, transforming an underperforming existing programme, or building the CRM strategies in banking required for a more personalised, data-driven customer engagement model.

Why Choose G&CO.?

G&CO. works with banking and financial services institutions to design the CRM strategies, loyalty programmes, and customer engagement infrastructure that build durable relationships and grow lifetime customer value. Through the Acumen platform, G&CO. provides the consumer and brand intelligence that ensures every loyalty investment and CRM decision is grounded in evidence about how each customer segment actually builds trust, makes product decisions, and responds to engagement.

Submit an inquiry to G&CO. on our contact page or click on the blue "Click to Contact Us" button on the bottom right corner of your screen for your convenience. We look forward to hearing from you.